Tax Season 2022 Now Open: Beware, This Year’s Deadlines are Shorter!

“Few of us ever test our powers of deduction, except when filling out an income tax form.” (Laurence J. Peter)

In this article, we look at the who, how and when of this 2022 Tax Season; highlight some issues that require special attention; and suggest practical next steps to help you avoid the last-minute rush, the risk of errors and omissions, and the cost of late submissions, penalties and audits.

At a glance

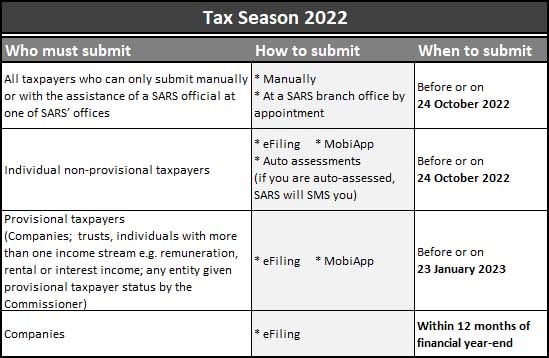

Tax Season 2022 opens 1 July 2022 – here is a quick overview of who must submit, how they must do so and when by:

Who is exempt from filing?

- Individuals receiving total annual gross income of less than R500,000 from only one source with no other allowances or benefits, and from whom PAYE has been deducted as per the prescribed tax deduction tables.

- Individuals who are not claiming tax related deductions or rebates such as medical expenses, travel and retirement annuity contributions other than pension contributions made by their employer.

- Individuals who only receive interest below the interest exemption thresholds; amounts from tax-free savings accounts; or dividends.

- Individuals who are non-residents throughout the year.

Even if you could be exempt at first glance you might still benefit from filing a return due to your particular circumstances. If there is any doubt, professional advice is essential.

Issues requiring special attention

- This year’s tax season is substantially shorter than last year’s for provisional, non-provisional, manual and branch office submissions!

Last year, non-provisional taxpayers had until 23 November, extended to 2 December at the last minute. This year’s deadline is a month earlier, on 24 October 2022.

Similarly, the 23 January 2023 deadline for provisional taxpayers is a week earlier. That’s less than seven months away, including the December and January holiday periods.

- Home office expenses remain in the spotlight, as SARS disallowed over 60% of home office claims last year. Make sure you qualify for this deduction, and that it is correctly pro-rata calculated for allowable non-capital expenses such as rates and taxes, electricity, repairs and insurance. Deductions can’t be claimed for reimbursements or equipment provided by an employer without charge. Also be sure to understand the potential capital gains tax impact when you sell your home for which the deduction was claimed. Professional advice is essential here!

- Last year more than three million taxpayers were auto-assessed, and significantly more individual taxpayers will be auto-assessed this year. If you are auto-assessed, SARS will send you an SMS that your tax return has been pre-populated by SARS on eFiling or the SARS MobiApp. Check with your accountant before making any decisions about your auto-assessment.

- Be sure to check if your auto-assessment is correct as soon as you receive the SMS notification, because this year there is no need to “accept” the assessment: SARS will regard it as accepted unless changes are made as detailed below before the 24 October deadline. If an amount is due to SARS, the next step is simply to make the payment via eFiling or SARS MobiApp. If a refund is due to you, check that your banking details with SARS are correct and simply wait for the refund.If you don’t agree with the automated assessment, an accurate ITR12 tax return can be filed within 40 business days of the date of the auto assessment. If this return is filed after 24 October, it will be subject to normal late submission admin penalties and interest. If SARS accepts the changes, a reduced or additional assessment will be issued. If not, the normal objection and appeal options are available.

- SARS has stated that Company Income Tax (CIT) filing compliance is currently a focus and urges companies to note that it is compulsory for registered companies that are required to file a return to do so on time and complete in all respects.

- Non-compliance is as expensive as ever, with the same penalty rules for auto-assessments expected to apply for the 2022 filing season. The late submission admin penalty ranges from R250 to R16,000 a month for up to 35 months, depending on the assessed loss or taxable income of the taxpayer for the year prior to the year being assessed.

In addition, failure to submit the return(s) within the prescribed period could result in a summons and/or criminal prosecution, which upon conviction is subject to a fine or to imprisonment for a period of up to two years.

Next steps

- Get started immediately to avoid the last-minute rush, and to minimise the risk of errors and omissions. Diarise the key dates, allowing time to attend to any potential problems, such as finding documents, obtaining third party information or getting professional advice.

- Ensure all your information is correct. Update your personal information such as banking details, address and contact details on eFiling or the SARS MobiApp, and make sure all information provided on the return is true. SARS has significantly improved its abilities to draw information from third parties, including employers, financial institutions, medical schemes, retirement annuity fund administrators and other third-party data providers, making it easier than ever before for SARS to detect incorrect or undisclosed information.

- Check that you have received certificates and documents relevant in determining your tax obligations such as your IRP5/IT3(a)s and other tax certificates like medical certificates, retirement annuity fund certificate and other 3rd party data. If not, immediately contact the 3rd party data provider.

- Keep accurate records of all the calculations and source documents used as SARS may ask for these documents to be verified and/or for the calculations to be justified.

- Consider professional assistance to ensure all exemptions, rebates and deductions for businesses and individuals are included and that the many terms and conditions, dictating when and how these may be claimed, have been met. Last year, SARS refunded more than R17 billion to taxpayers.

- Plan ahead financially to meet the tax liability that will be due along with the submission deadline.

Owe SARS a Tax Debt? Here Are Your Options…

“Tax debtors are expected to take responsibility for their tax obligations and to organise their affairs in such a way as to be able to discharge those responsibilities when required. They should give at least the same priority to tax obligations as their other responsibilities.” (SARS’ Short Guide to the Tax Administration Act)

To avoid tax debt, penalties and interest, it is best to file returns and make payments timeously. However, for a range of reasons, taxpayers may not be able to meet these requirements on time, finding themselves facing a tax debt owed to SARS.

There are different ways in which tax debt can arise, and while the taxpayers’ agreement and ability to settle this debt will determine the details of each taxpayer’s response, all tax debts should be handled the same way: promptly and with professional assistance.

If you or your company have any tax debt, take action without delay! In certain circumstances and with the right professional assistance, an agreement may be reached with SARS to defer the tax debt for later payment or for payment by instalments.

How do tax debts arise?

Tax debts can arise from administrative penalties on late or non-submission of tax returns, failure to submit tax returns, the submission of returns without payment, partial payment of a tax liability or from a SARS audit assessment.

How would you know about a tax debt?

Individuals and businesses should – proactively and on a regular basis – check their compliance status with SARS or obtain a statement of account on the various taxes payable, either from their accountant or via the SARS’ Contact Centre, eFiling and the SARS MobiApp, to confirm if SARS is owed any amounts.

SARS is also required to inform taxpayers of assessments, notifications or communications issued, by also sending a message to a taxpayer’s last known number or email address. This makes it crucial to keep your contact details updated at SARS and to check your compliance status or statement of account whenever an email or SMS is received from SARS.

No dispute, but can’t pay now?

In many cases, a taxpayer may not dispute the existence or amount of a tax debt but is unable to meet the payment required by the stipulated date.

In this case, there are two options that could be considered based on the unique facts of each case.

- The first is a payment arrangement

SARS provides for a deferment, or instalment payment arrangement, for the outstanding tax debt. Taxpayers can request and enter into an instalment payment arrangement with SARS that allows the outstanding debt, including applicable interest, to be paid in one sum or in instalments over time (up to 36 months). This agreement is subject to certain qualifying criteria, for example, the payment arrangement must cover the entire debt and all non-compliance must first be remedied, which means all returns and/or recons must be correctly submitted.

Until recently, taxpayers could only make payment arrangements via a debt collector who had been appointed by SARS, in person at a SARS branch, utilising the debt management regional email addresses, or on the My Compliance Profile (MCP) on eFiling.

SARS recently implemented the Enhanced Debt Management process to help taxpayers with outstanding debt initiate a request for Payment Arrangement for Personal Income Tax (PIT); Corporate Income Tax (CIT); Value-Added Tax (VAT); Pay-As-You-Earn (PAYE) and administrative penalties via eFiling.

If granted, the repayments are loaded via eFiling to be released from the taxpayer’s bank account. Interest will continue to accrue on any unpaid debt, and any breach of the conditions will terminate the payment agreement and normal collection proceedings will resume.

- The second is a compromise agreement

Applying for a compromise agreement is an option of last resort when a taxpayer cannot afford to settle the tax debt owing to SARS. A SARS Debt Compromise is a process whereby a taxpayer requests that SARS permanently or temporarily “write-off” a large portion of their debt, with the balance being paid in full by the taxpayer immediately on the condition that the taxpayer complies with any conditions imposed by SARS.It is important to note that a temporary write off is generally merely a suspension of the recovery of a debt, and the debt may still be recoverable during the prescription period which, under the Act, is 15 years.

In deciding to grant a compromise, a senior SARS official must have regard to several factors. However, no compromise will be granted in several instances, for example, if the taxpayer’s other tax affairs are not in order or where a taxpayer recently had a previous compromise agreement with SARS.

A compromise also cannot be considered if the taxpayer disputes the debt. If a matter is under objection or appeal, the taxpayer must withdraw the objection or appeal before a compromise can be considered.

If you are looking for a compromise with SARS, professional assistance is crucial.

Disputing a tax debt?

Often, taxpayers disagree with assessments issued by SARS. While taxpayers do have the right to dispute an assessment by lodging an objection, it is vital to note that an objection or appeal lodged with SARS does not in any way suspend or postpone the payment of the tax debt.

Aptly named the “pay-now-argue-later” principle, it applies to all tax debt.

To prevent SARS from instituting collection proceedings on a tax debt that is to be disputed, two steps are required:

- Lodge an objection in dispute of the assessment AND

- Submit a “Request for Suspension of Payment.”

The taxpayer is protected from all SARS collection procedures between the dates that SARS receives the request, to 10 business days after SARS issues its decision to grant or decline the Suspension of Payment request.

A Suspension of Payment request can only be granted by a senior SARS official, after taking into consideration several factors, including the compliance history of the taxpayer and whether the dispute is a result of fraud.

If a Suspension of Payment request is granted, SARS may not commence any collection proceedings for the tax debt in dispute pending the outcome of the objection or appeal. However, interest will accrue on the unpaid debt.

If SARS denies the Suspension of Payment request, the taxpayer also has the option to apply to SARS for a payment plan. A Suspension of Payment is also revoked if the dispute process is not followed.

On the finalisation of the objection or appeal, a revised assessment will reflect the resulting tax debt and the due date for payment. Again, if the revised tax debt is not paid on time, SARS may commence collection proceedings.

Why you must act promptly and professionally

It is a criminal offense to not submit a tax return when it is due, and it can be a criminal offense not to pay.

If you cannot pay a tax debt to SARS and do not follow the correct procedures, SARS is legally allowed to exercise its wide powers of collection. However, SARS states that when deciding the most appropriate way to deal with outstanding tax obligations, it will give considerable weight to the tax debtors’ individual circumstances and compliance history of, for example, lodging correct returns and documents and paying taxes on time.

SARS’ debt collection powers extend to issuing a judgment and having a taxpayer blacklisted; obtaining a preservation order in respect of taxpayer assets; attaching and selling taxpayer assets; and bringing sequestration or liquidation proceedings against a taxpayer, even if the debt is disputed. In fact, even the money in your savings account or your income may be in jeopardy.

This is because SARS can access data in relation to every bank account registered in your name using your ID number and can also recover tax debt through third parties who hold money on your behalf, such as a bank, an employer, an insurance company or an attorney.

Due to recent changes to the tax laws, there have been increasing reports of SARS collecting ‘outstanding tax debts’ from taxpayers’ bank accounts, without the taxpayers’ consent. While SARS can indeed do this without any judicial oversight, it is important to know that SARS is required by law to follow specific steps prescribed by the Tax Administration Act (TAA) before doing so.

These include that the taxpayer must have received an assessment from SARS detailing how much is due and by when, as well as a final demand for payment that states available debt relief mechanisms contained in the TAA; and recovery steps that SARS may take if the tax debt is not paid. Taxpayers who can prove serious financial hardship may apply to SARS for a reduction of the amount within 5 business days of receiving the final demand or extend the period over which the amount must be paid.

Only 10 business days after delivery of the final demand, if no response has been received from the taxpayer, can a senior SARS official authorise a third party to collect the tax debt. However, if SARS does not follow the steps detailed in the TAA, collection proceedings may be regarded as illegal and in contravention of the TAA, and the taxpayer will have recourse against SARS via its Complaint Management Office (CMO), the Tax Ombud or legal action. Again, in these instances, professional assistance is strongly recommended.

Keep Your Business Simple!

“Simple can be harder than complex: You have to work hard to get your thinking clean to make it simple. But it’s worth it in the end because once you get there, you can move mountains.” (Steve Jobs, co-founder of Apple)

It is easy in business culture to start believing that more is more. Entrepreneurs often fall into the trap that more meetings, more employees, more products and more leads is equal to more success. Many large companies have failed because they branched out too much, lost focus and, as a result, lost their market.

Quite often the idea that bigger is better and more is more can lead to poor decision making that guides a business away from its competitive advantages, confuses the market and leads to a lack of focus internally. The flip side of this is the ability to strip back unnecessary complexity and instead focus on simplicity.

Simplicity is defined as “the quality or condition of being easy to understand or to do” and it comes with some genuine advantages.

The advantages of simplicity

- Being understood

The major advantage of simplicity is that it makes it easy for everyone in your organisation to be on the same page. Having everyone understand the goals and ambitions of an organisation is easier when you are a small company, but as things develop it becomes increasingly difficult to get everyone pulling in the same direction.Removing jargon and chaff from company communications, and simplifying product offerings, your vision, team structures and communication will ensure that not only do your team know what they are doing day-to-day to achieve success, but also that they know how to do it.

Once your whole company is singing from the same hymn book it’s far easier to get the world at large to understand what you are doing too, which makes defining your brand and selling your products a simpler proposition at the same time.

- It’s easier to operate

The more things that have to happen right for your business to succeed, the greater the risk. Keeping your business practices simple; from the number of suppliers to the levels of training needed by your staff will help you avoid the problems that complexity can bring. If you have thirty suppliers, it takes only one of them to fail to start impacting your business.|On the other side, if you have one supplier of a common product that can be sourced somewhere else, it’s much easier to keep a handle on your production line and ensure that you always have the products you need. (Of course, you do not want to be reliant on a sole supplier without the option of other sources for your essential resources). Obviously, this is an extreme example, but it will never hurt to go through your supplier lists, staffing or any other factor of your business and look at where the number of cogs can be reduced.

Also, with a select group of suppliers, it will be easier to keep informed of their health and sustainability and ability to continue supplying your business regularly and on time.

- It’s adaptable

A simple business model is much easier to adapt should the need arise. A simple business with easy-to-understand communication lines and supply chains is easier to pivot because staff can all be contacted at once and updated, while supply adjustments can be adapted as needs be on the spot. - Results are easier to measure

Overly difficult strategies are harder to implement, and they also make it harder to gauge results. It is far harder to work out which staff and departments are delivering the most value in a company when you have two dozen departments with different KPIs and a hundred staff each than it is in a small company with just a handful of staff. The most successful companies have a straightforward direction, along with clear and simple measuring parameters that keep them on track.If, however, your operation has grown into a business with a number of divisions, apply these tips for simplification to each division to encourage their efficient and effective performance.

Tips for simplifying your business

Ironically, making a company easy to understand and operate is not necessarily an easy thing to do. Getting to grips with where changes need to be made will take some time and will require bold decision making. Here are our tips for keeping things simple in your business.

- Outline your goals

Whether you want to reduce waste, increase employee happiness, or boost profitability, simplifying your business should always start with defining your goals. This should be a short list that allows you to more clearly understand and communicate just what is being tackled and why. Having a short list makes it much more likely that it will get completed without burdening staff further, and also allows you to easily see if the process has been successful.Having simple, clearly defined objectives and goals, that the whole team understand and commit to, gives the business the best possibility of success.

- Consider the outsider’s perspective

There is no doubt, if you lead a business, that you know what it is you are offering and just how many ways you offer it. Being in this position of full understanding can, however, mean that you have lost track of what the average person, or woman, on the street thinks it is you do. Looking at your company from the perspective of an outsider is therefore important if you want to get a sense of how your company and brand are perceived.The easiest way to do this is simply to ask. Ask customers, ask friends, ask people at business meetings, or, if you are a larger company, hire a company to do a survey or bring in a consultant. Getting other people’s opinions will quickly show you if you have lost track of your core business. If there is confusion about what you do, or what your primary services are, then it’s a sure sign you may need to go back to basics or change the messaging around your company.

At the same time, ask your customers what they really want. The answers may surprise you and reveal areas where you have been putting in a lot of effort that doesn’t necessarily give the customers what they actually need. This is an essential exercise to determine the continuing relevance of and need for your service offering or product. Change is an ever-increasing factor and new products and services are coming to market. Keeping your business focussed and simple can enable recognition of the emerging threats and need to change, adapt or even develop new offerings.

- Focus on outcomes

While it may be tempting to watch every move every employee makes, doing so is a hugely time intensive activity that adds layer upon layer to the complexity of a business. Instead of simply hiring someone to do the job, you are now hiring people to supervise and check up on them, and to do that requires more HR functionality to manage all their expectations. Your focus should be on performance outcomes of your key employees.Additionally, not all rules and regulations will assist your company and these need to be looked at carefully if you want to streamline workflows and increase employee job satisfaction and retention. Look, for example, at how many people need to review and sign off on expense reports or small purchases; or how many times slide decks need to be reviewed before they are presented.

Reducing menial tasks and making things easier to do gives employees more time to actually do their real jobs properly. The answer to all of this is to focus on outcomes and avoid micromanaging your team. Be sure to maintain an open line of communication with the understanding that the more you listen to your team, the simpler things will be and the better the entire group will work. In addition, being accessible and listening to your people will alert you earlier to emerging risks and potential opportunities in time to take action.

This is going to extend to your ability to hear bad news or have employees tell you when they think your decisions may be wrong. You are only going to find out about bad practices and unclear instructions if you are genuinely interested in fixing problems rather than protecting egos.

- Fix your non-functioning processes

Whether it’s because you have been in operation for so long that your processes have become redundant or because you are just starting out and haven’t developed any, having non-functioning processes can hamper your workflow and cause a huge amount of unnecessary and time-consuming work.The first step is identifying your pain points. Start with the areas of the business where you are actively getting complaints. Break down what processes are leading to these complaints and fix them. The time you spend developing good practices will be more than paid back in the decreased amount of time you spend putting out fires and dealing with unhappy customers. Ultimately, you will want to look at all your processes to make sure they are running optimally, and that time isn’t being wasted unnecessarily dealing on a daily basis with inconvenient problems that could be solved outright.

- Organise administration assistance

Administration is a necessary but unfortunate consequence of doing business that can clog up all the otherwise smooth flowing systems. You did not hire those important and highly educated staff to have them sit filling in order forms. You and they should be focused on driving the business, not dealing with payment complaints. Whether you choose to use automated assistance that frees up a researcher’s time in a laboratory, an accountant to organise your finances and save you money on your taxes or someone in HR to deal with errors in pay, getting others to do the finicky work will allow your core team to focus on what they need to do to bring in the profit. Keep management of operating/production teams simple. In the long run, the time saved for everyone will turn into a smoother, and more efficient company.

At the end of the day, simplifying a company is about getting to the core of what it is you need to do, supplying customers with exactly what they need and no more, making sure your staff are well informed and working together and not overburdened with work that isn’t their place to do.