“A trust is a ‘person’ for tax purposes and is therefore a taxpayer in its own right.” (SARS)

SARS recently sent out a reminder confirming that in terms of the Income Tax Act, 1962 (ITA), all trusts are taxpayers and that the trustees, who are also the representative taxpayers of the trust, have a responsibility to register the trusts – whether active or dormant – for income tax purposes.

The representative taxpayer (trustee/s), or the appointed tax practitioner, must also file an income tax return for the trust on an annual basis, and before the tax season deadlines to avoid penalties and interest.

Trusts that are required to register include all local trusts, non-resident trusts that are effectively managed in South Africa, as well as non-resident trusts that derive income from a South African source.

Why business owners use trusts

Trusts are used to hold, protect and ensure the continuity of ownership of personal or business assets, shares in businesses, and the right of use of assets.

The benefits include protection of assets against creditors, for example in the case of liquidation or sequestration, and against other parties – for example an ex-spouse, or ill-intentioned family member.

Where appropriate, a trust can be a useful tool to help ensure effective future planning; achieve continuity through efficient succession; and even managing certain tax liabilities, such as estate duty.

A business can also be registered in a business trust, also called a “trading trust,” instead of registering as a company with the CIPC. This option, however, is only appropriate where the main aim is conducting business, and a contractual agreement will task the trustees to manage the assets of the trust for a profit.

While a business trust can be useful to protect assets and safeguard the business owner against certain liabilities, it also has several drawbacks and may not always be the right alternative to registering a company.

Whether a business or personal trust, professional advice and guidance is crucial, because not only are the rules governing trusts complex, but the taxation of trusts requires specialised expertise.

The taxation of trusts

Whereas companies in South Africa are taxed at a flat rate of 27% for years of assessment ending after 31 March 2023, the income tax rate for trusts is currently 45%, and it is levied on any income retained in the trust.

This is the highest income tax rate, and trusts also do not qualify for any of the rebates provided for in Section 6 of the Income Tax Act.

Trustees may allocate income and capital to multiple beneficiaries, so that the tax obligation is spread, possibly at a lower rate in some instances. This is because, depending on circumstances, income distributed may be taxable in the hands of the founder, the beneficiaries or the trustees.

There are also special trusts, taxed at a sliding scale of 18% – 45% (the same as natural persons), and some special trusts also qualify for certain relief from Capital Gains Tax.

How to submit a tax return for your trust

It sounds quite simple in theory: an ITR12T must be completed and submitted.

In reality, a ITR12T trust tax return is a 31-page document, and completing it correctly is no quick or easy task.

Firstly, a trust must be registered with SARS for the taxes for which it may be liable. In addition, the trustees of the trust – who are also the representative taxpayers of the trust – must file the return within the tax season deadline. This responsibility may be conferred to a specific trustee, or to a professional appointed by the trustee(s).

To make it easier to comply, SARS has announced some enhancements to its system. For example, whereas one could previously only register a trust via a visit to a SARS branch, taxpayers can now register a trust for tax purposes through the SARS Online Query System and also submit any supporting documents online.

Furthermore, the ITR12T trust return form is now available on eFiling. The representative of a registered trust can request the return on eFiling and customise it by completing the questions on the Tax Wizard. Requesting the ITR12T to be posted, as was previously required, is no longer an option and trust returns received via post will be rejected.

Taxpayers registered for eFiling are also able to complete and submit the return online. Only trusts with ten or fewer beneficiaries have the option to have the ITR12T return captured by a SARS agent at a branch, and only if an appointment has been made.

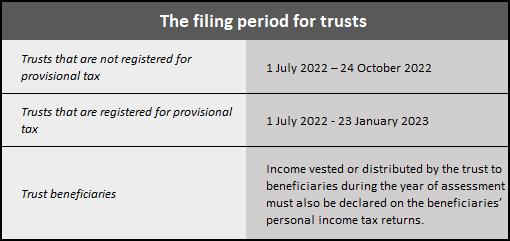

When the filing period for trusts ends, SARS will raise original estimated assessments on ITR12Ts that were not officially filed by the taxpayer.

After the estimated assessment has been raised by SARS, the taxpayer will be allowed to request an original (new) return to be submitted to SARS. The same estimated return will be issued on eFiling to be completed, with a new version number of the return.

The taxpayer will be able to request a correction after the original return has been submitted, until one or two rejection letters have been received from SARS. Thereafter, the taxpayer will have the option to dispute the decision taken by SARS.

Bear in mind…

- SARS introduced a number of form and system changes in respect of trusts from 24 June 2022.

- SARS has advised trusts that all outstanding income tax returns are submitted without delay to avoid further penalties and interest.

- SARS reminds trusts not registered for income tax purposes of the availability of the Voluntary Disclosure Programme (VDP), an option that should only be considered after obtaining professional advice.

- If the ITR12T return is not submitted by the relevant deadline, the trust will be liable for an administrative penalty due to non-compliance.

- Provisional taxpayers are required to make provisional tax payments within six months after the commencement of a year of assessment and then again by the end of the year of assessment.

- The trust is required to keep all the relevant material and supporting documents for a period of five (5) years from the date of submission of the return. SARS may, within the 5-year period, request these documents to verify the information that was declared on the ITR12T.