Your Tax Deadlines for July 2026

- 07 July: PAYE submissions and payments

- 24 July: VAT manual submissions and payments

- 30 July: Excise duty payments

- 31 July:

-

- VAT electronic submissions and payments

- CIT Provisional Tax payments where applicable

“The bottom line is that having a purpose is good business. It is the business of the future.” (Brian Whipple, former CEO of Accenture Song)

In 2026, Gen Z and Millennials are beginning to take their place as the dominant purchasing generations. It’s a significant moment as these two generations do things differently to those that came before. Millennials established the trend, choosing to focus on values-led purchasing, driven by a preference for transparency, and a willingness to hold brands to account. Gen Z has taken it further still, treating consumption as activism.

According to McKinsey & Company, nearly 70 percent of respondents say that a brand’s social and ethical values directly influence their purchasing decisions. This deepening sense that spending choices carry moral weight, a trend known as “charitable identity”, has created a consumer bloc unlike any that has come before it. For small business owners and entrepreneurs, understanding this shift is about to become essential for future earnings.

For older generations, brand loyalty was largely built on reliability and price. For younger consumers, the framework is entirely different: brands are worn like values on a sleeve. Research from the 2024 Edelman Trust Barometer confirms that Gen Z uses brand affiliation as a form of social signalling. It’s a way of communicating who they are, and who they are not. This means that choosing to buy from a brand is less about the product and more about the statement. A clothing label with verified ethical supply chains, a bank that invests in community lending, or a coffee company that pays fair-trade premiums: these are all brands that allow the purchaser to feel that their money is doing something meaningful. In this sense, purpose-driven brands have become a form of charitable giving. The consumer simultaneously acquires a product and signals support for a cause.

Perhaps the most nuanced dimension of this trend is the ever-blurring line between consumption and philanthropy. For many younger consumers, donating to a cause and buying from a purpose-aligned brand are not distinct activities. They occupy the same emotional register: both feel like acts of conviction.

This overlap between consumption and charitable intent is transforming the way small businesses can position themselves: a clear social mission is also a business goal. If you have not made space in your annual budgets for your social mission, this must be rectified as soon as possible. You need to decide just what you stand for, and how much you can afford to invest in this aspect of your business. As your accountants, we can help you with this.

Getting involved in initiatives like Mandela Day is no longer a purely philanthropic choice. And, interestingly, small businesses have an advantage over big ones. While a large corporation can sponsor a global cause at arm’s length, a small business can muck in at a local level. From supporting the local school’s sports team, volunteering at a food bank, or committing a percentage of monthly sales to a neighbourhood cause, it’s all about making your values visible to your immediate community.

Regular and authentic charitable activity generates word-of-mouth referrals that no advertising budget can replicate. It earns coverage in local and trade media, and produces social media content that resonates precisely because it is real. It also builds internal loyalty, as employees who feel proud of where they work are more motivated and less likely to leave.

The key piece, however, is alignment. Charitable activity that feels disconnected from your business’s identity will stick out to a generation trained to detect inauthenticity at a glance. A legal firm that mentors disadvantaged youth, an accountancy practice that runs free financial literacy workshops, a café that donates unsold food to a local shelter: these are acts of giving that simultaneously tell a coherent story about who you are and what you stand for.

The practical formula is straightforward: choose causes your team genuinely cares about, build long-term partnerships rather than one-off gestures, communicate them consistently across your channels, and track the outcome not only in goodwill but in customer retention and referral rates. What you choose to do for Mandela Day is a valuable part of your brand, not just an excuse to get out of the office.

“Small is not a stepping stone. You can move. You can adjust. You can adapt. You can get it done while they’re still stuck deciding what to do.” (Jason Fried, entrepreneur and author)

When starting a small business, it’s easy to assume you don’t have all the knowledge you need to compete, and that the big, successful corporation next door holds all the keys to success. With their polished org charts, complex strategy documents, and fleets of middle managers, big corporations and their strategies can look like growth to the beginner.

This is a mistake. The truth is, big companies operate within a completely different set of constraints and economies to smaller, founder-run businesses. Understanding which big business strategies could hurt if implemented in your business, is therefore a key to survival.

Large corporations often hire ahead of demand. They build out departments, create roles to fill future needs, and staff up in anticipation of growth. They can afford to carry headcount. Smaller businesses cannot.

Many small business owners get caught up in the excitement of expansion, and start hiring to look like a bigger company, or in anticipation of future problems, rather than to solve a specific current issue. They add a layer of management before there’s anything to manage, or recruit a marketing team before they’ve validated what their customers actually want. The result is a payroll that grows faster than revenue, and a business that starts to take strain under the weight of salaries it was never ready to carry. As a new business, it is essential that each hire adds immediate value to the company and can justify their pay cheque from day one. If you are unsure what someone will do in their first 90 days, this is probably a hire you don’t need.

Big companies love processes and reporting structures. Everything from ordering printer paper to launching a new product needs multiple meetings, committee sign-offs, and documented procedures. Some of this is necessary when you’re coordinating thousands of people across continents… But for a small team, your biggest advantage is agility.

Small businesses thrive on speed and flexibility. Your ability to make a decision at 9am and implement it by lunchtime is a genuine competitive edge over a corporate rival that needs a risk assessment before it can switch toilet paper suppliers. The moment you start building bureaucracy into your own operation (think overly formal sign-off chains, or meetings about meetings) you are denting the very quality that makes you competitive.

A classic mistake many growing startups make, is one that’s also obvious to any experienced business owner the second they walk into the offices. The expensive logo on frosted glass, the branded hoodies, and the slick website are all in evidence – but the pipeline runs thin and the cash flow statement speaks of desperation.

Big companies invest heavily in brand because they have proven revenue streams and established customer relationships. Brand maintenance is a legitimate line item at that scale. For a small business still finding its feet, over-investing in brand before you have a viable business is putting the cart firmly before the horse. Customers care more about whether you solve their problem better than anyone else than they do about your brand. Earn that reputation first. The brand follows from the substance, not the other way around.

Publicly listed companies are accountable to shareholders who want to see top-line revenue growth. That pressure filters through to every level of a large organisation and shapes how it measures success. Revenue is celebrated; profit is secondary. For small and medium-sized businesses, this is a genuinely dangerous mindset to adopt.

In the early days, cash flow will be the ultimate difference between thriving and going bang. A client can owe you a large sum and your business can still fail if that money doesn’t arrive in time to cover your wages run.

But still, small business owners routinely chase headline revenue figures, winning bigger contracts, and pursuing growth at all costs without doing the hard work of understanding whether these sales are actually translating into cash flow, and whether the timing of receipts matches the reality of their outgoings. It is vital that you know the real numbers that will affect the day-to-day running of your business. And that you understand the difference between revenue and profit, and between profit and cash in the bank. As your accountants, we are here to help you see this clearly.

Enterprise businesses outsource customer service, because economies of scale demand it. For small businesses, this is a critical error, as the relationship between your business and your customers is one of the most valuable assets you possess.

When you outsource your pitches to a big agency, your customer queries to a call centre, or your social media to a junior member of staff who doesn’t really understand what you do, you lose the intimacy that made customers choose you in the first place. People buy from small businesses because they feel seen. They want the expert, not the system. Protect that connection carefully.

The bottom line is this: the best small businesses succeed by doing things that big companies structurally cannot. They move fast, know their customers personally, make smart decisions without bureaucracy, and treat every rand as precious. Lean into that while you still have it.

“All trusts established in South Africa are required to register with SARS, regardless of whether they have any transactions or income.” (SARS)

When Mr and Mrs J set up a Type-A special trust for their eldest son, who is intellectually challenged, their intention was to make certain there would always be sufficient financial resources for his best care, both during and beyond their lifetimes. A special trust was recommended by a professional advisor and with good reason: Type-A special trusts are created “solely for the benefit of a person with a mental or physical disability.”

However, as Mr and Mrs J found out, while Type-A special trusts have very compelling tax benefits, there are also substantial tax limitations. Fully understanding these within the unique personal context of the ultimate beneficiary is essential to ensuring the trust objectives are met over the long-term. And that means relying on specialist and individualised tax advice when considering a trust arrangement of any kind.

A correctly structured trust can be a powerful financial planning tool for business and property owners, wealthy individuals, or families. It can help manage succession, protect assets, provide for children or dependents, navigate estate planning issues and pass on wealth responsibly.

What is crucial is setting up the right structure for the objectives of the particular trust and understanding the consequences – and particularly the tax consequences – of the decisions made.

There are many different types of trusts in South Africa. For example, an inter vivos (living or family) trust, is created during your lifetime to hold assets such as property, business interests or investments, while a testamentary trust is created through a will (it only kicks in after your death) and is especially important where minor children are involved.

There are also vesting and discretionary trusts, and hybrid trusts that combine the two, as well as a range of specific application trusts like trading (business) trusts, charitable trusts or BEE trusts, to mention but a few.

For tax purposes, two types of special trusts are also recognised, the Type-A special trust is intended solely for a person with a mental or physical disability, as in our opening story, and the Type-B special trust created specifically for the benefit of relatives of a deceased person, provided at least one beneficiary is a minor on the last day of the trust’s year of assessment.

The trust types are not mutually exclusive. For example, a trust can technically be both a Type-A special trust and a vesting trust; or both a Type-B special trust and a discretionary trust.

However, the exact trust type really matters from a tax perspective, because Type-A and Type-B special trusts are not taxed in the same way, and both are taxed differently to normal trusts. This should be carefully considered before establishing a trust, and then disclosed when completing the mandatory annual tax returns.

In terms of what is called the “conduit principle”, trust income or capital gains may be taxed in the hands of the trust or the beneficiaries, depending on when that income or capital gain vests.

Where the trust itself is taxed, it is taxed at a flat rate of 45%. Beneficiaries are taxed at their personal tax rate on a sliding scale from 18% to 45% and also benefit from various tax rebates. SARS taxes a trust’s capital gains depending on whether the gains are retained in the trust or vested to a beneficiary in the same year of assessment. Normal trusts face an effective Capital Gains Tax (CGT) rate of 36% (calculated from an inclusion rate of 80%, which is then taxed at the flat 45% income tax).

Beneficiaries that are individual taxpayers have a maximum effective CGT rate of 18% (calculated from an inclusion rate of 40%) and also qualify for rebates such as the R50,000 annual CGT exclusion, the R3-million primary residence CGT exclusion, and disregarded CGT gains on personal-use assets or compensation for personal injury, illness or defamation.

Type-A special trusts, on the other hand, are taxed using individual income tax brackets on a progressive sliding scale from 18% to 45%.

Their capital gains inclusion rate is 40%, making their maximum effective CGT rate 18%, lower than for normal trusts and the same as for natural persons. They also qualify for CGT rebates that apply to individuals as listed above. Relief from donations tax on interest-free or low-interest loans to Type-A special trusts also applies.

However, there are some important tax limitations. Type-A special trusts do not qualify for medical tax credits, primary tax rebates, or the annual interest exemption available to natural persons. A Type-A special trust may vest income in a qualifying beneficiary so that the income is taxed in that individual’s hands, enabling the individual to use their own rebates, medical credits and interest exemption.

Bottom line: it’s complicated, so get professional tax advice based on your specific circumstances.

Whether you’re considering a special trust, an inter vivos trust, or any other structure, the differences in how income and capital gains are taxed, and what tax rebates are allowed, can have a significant impact on the real-world benefit delivered to the trust beneficiaries. The right choice depends entirely on the trust’s objectives, your unique circumstances, and a careful analysis of possible tax consequences.

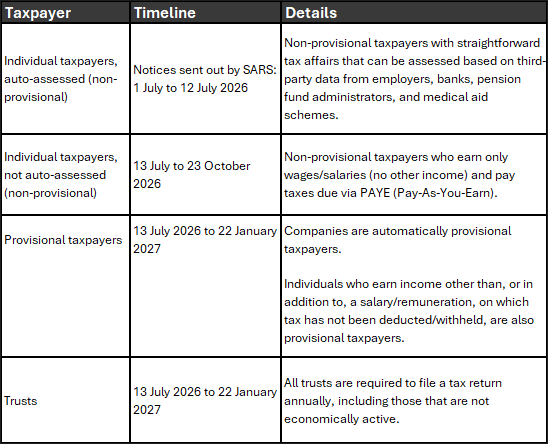

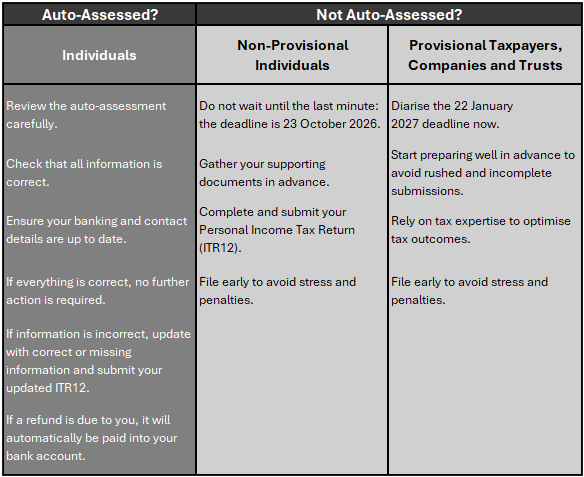

“The Power of Done starts with knowing when to act.” (SARS)

The 2026 Tax Season officially opens on 13 July 2026 for the 2025/2026 year of assessment, covering the period between 1 March 2025 and 28 February 2026.

During filing season, taxpayers must complete and submit their tax returns, declaring their income and deductions to allow SARS to determine their final tax liability for the period under assessment.

This is what we can do for you:

SARS has significantly increased its scrutiny of trust administration. What’s more, from the beginning of May 2026, automated administrative penalties apply to all non-compliant trusts – without exception.

Whether a trust is active or dormant, the trustees have a legal obligation to comply with SARS requirements, and the consequences of failing to do so are now immediate and ongoing.

All trusts must:

Trustees act as representative taxpayers of a trust in terms of the Income Tax Act and personally bear sole responsibility for ensuring full compliance.

This includes maintaining accurate trust information, ensuring that all legal and tax obligations are met, and initiating deregistration processes for trusts that meet the applicable criteria.

From 4 May 2026, SARS will issue a penalty assessment notice for all outstanding trust income tax returns for tax periods from 2024 onwards.

Designed to encourage compliance, these penalties are applied consistently, recurring monthly until non-compliance is corrected. Monthly administrative penalties may range from R250 to R16,000 per outstanding return, depending on the trust’s taxable income for the preceding year and will accumulate until the non-compliance is corrected, up to a maximum of 35 months.

It doesn’t stop there. SARS may in specific circumstances hold trustees personally liable for the trust’s tax debts, and trustees are individually and jointly liable for the trust’s tax compliance.

In addition, non-compliance with SARS obligations may be regarded as a criminal offence and will attract penalties and interest. Trustees who fail to act face penalties, interest, and potential criminal charges.

SARS requires all registered resident trusts, without exception (and certain qualifying non-resident trusts), to meet the range of ongoing obligations.

A trust’s tax compliance obligations only come to an end once it has been formally deregistered with SARS. Until this process is finalised, the trust remains active for tax purposes and is exposed to penalties for continued non-compliance.

Where a trust is no longer being used for its intended purpose, trustees are encouraged to formally terminate the trust. The first step is to regularise the trust’s tax affairs by submitting all outstanding returns, settling all tax liabilities, and updating all trust information.

Thereafter the trust can be formally terminated through the Office of the Master of the High Court. Once the Master has issued written confirmation of termination, trustees can ask SARS to deregister the trust for income tax purposes.

“Leaders must either invest a reasonable amount of time attending to fears and feelings, or squander an unreasonable amount of time trying to manage ineffective and unproductive behaviour.” (Brené Brown, Dare to Lead)

Running a business is a human endeavour, and as such, every business leader will eventually find themselves faced with a skilled, reliable employee who starts showing signs that something is deeply wrong outside of work. Maybe their performance dips suddenly, or perhaps they’re distracted, tearful, or inexplicably short-tempered? Maybe they even come to you directly and share something deeply private? In that moment, you’re no longer just an employer managing output and payroll. You become, whether you’re ready for it or not, a human being navigating someone else’s pain. The way small business owners handle these moments has a profound effect not only on the individual concerned, but on team morale, workplace culture, and the long-term health of the business itself. Here’s what you need to do.

The first, and often hardest, step is simply opening the door. Many managers notice something is wrong but say nothing, hoping it will resolve itself. If you observe a genuine change in an employee’s behaviour or performance, it is important that you request a quiet, private meeting and approach it gently.

Avoid framing it as a performance issue at this stage. Instead, lead with concern, “I’ve noticed you haven’t seemed yourself lately. Is everything okay?” That single question can be transformative. It signals that you see the person, not just the output. During this conversation you should simply listen, acknowledge what you are hearing and resist the temptation to offer advice or opinions. In short, be a decent human rather than a boss.

Once you understand the situation, it’s important to consider both your legal responsibilities and your personal boundaries. Depending on the nature of the crisis, you may have obligations around statutory sick pay, flexible working requests, or reasonable adjustments. Reread your employment contracts and HR policies. If your business doesn’t yet have clear wellbeing policies, this is a timely moment to create them. We will be able to help you establish budgets for contingencies such as freelancer assistance or added sick leave.

Equally, be honest with yourself about what you can and cannot provide. You are not a counsellor, and it is neither fair nor appropriate to position yourself as one. Pointing the employee towards professional support, your Employee Assistance Programme if you have one, or external resources is neither cold nor unreasonable.

Once the initial conversation has taken place, work collaboratively with your employee to agree on a short-term plan. This might involve a temporary reduction in hours, a period of remote working, adjusted responsibilities, or a phased return following their absence. The key word here is collaboratively. Imposing a solution, however well-intentioned, can feel patronising and could risk legal issues. Asking what would help communicates respect and encourages autonomy at a moment when the person may feel they have very little control over their own life. Document whatever is agreed, not to create a paper trail, but to give both parties clarity and to prevent misunderstandings further down the line.

Whatever an employee chooses to disclose, they are placing enormous trust in you. Do not share the details of their situation with colleagues or outsiders, even with the best intentions. If their absence or change in role requires some explanation to the wider team, keep it vague: “[Name] is dealing with a personal matter and we’re supporting them through it.” That is sufficient. Even well-meaning gossip can be devastating to someone already feeling vulnerable. And it also sends a powerful signal to every other member of your team about how their own confidences might be handled in the future.

Once a plan is in place, maintain regular, low-pressure contact. A brief message or a five-minute conversation every week or two shows continued care without adding pressure. There is a meaningful difference between checking in and checking up, which can feel like surveillance. As time passes, gently begin to reintegrate normal expectations, always communicating changes clearly and compassionately rather than simply shifting the goalposts.

Employees who are supported through personal crises often emerge more committed, more resilient, and more loyal than before. That outcome doesn’t happen by accident. It happens because someone in a position of authority chose to lead with humanity.

“Small business success in this economy isn’t about the ‘next big thing’ in tech; it’s about the ‘next small thing'” (Isabel Guzman)

It’s no secret that doing business has undergone significant overhauls over the last few years. The invention of AI, and the backlash to it, have led to an increase in automation, and, in turn, a recognition that customers are now more likely than ever to value the personal touch. It’s a grand shift that might leave many small business owners uncertain just where they should be putting their energy. So how do you not only navigate this environment but actually come out more profitable?

Taking a close look at successful small businesses, it’s easy to see that there are three pillars that are often responsible for allowing independent owners to thrive in these difficult market conditions.

A clear trend has emerged where successful small businesses have started treating administrative tasks as a direct tax on their time and profit. Instead of hiring a part-time assistant or spending hours manually answering the same five questions on social media, owners are implementing “Admin-Zero” frameworks. This involves using micro-automation for customer FAQs, booking confirmations, and initial intake processes so you can focus on more personal and impactful areas.

The barrier to entry for these tools has collapsed. Even a single-chair barbershop or a mom-and-pop consultancy can now use AI-driven frameworks as efficient alternatives to conventional manual procedures. This means that employee time is being saved in countless small ways daily. Spending that time on more productive behaviour like nurturing networks or driving sales has exponential benefits.

Volatility is one of the primary enemies of small businesses. To combat this, many business owners are adopting “Service Club” memberships, a model that functions as “cash flow insurance.” Customers are being encouraged to pay a modest monthly fee to receive priority bookings, a small monthly perk, or an annual benefit or service.

This model shifts the customer relationship from transactional to relational. It ensures the business remains top-of-mind for the consumer while providing the owner with a financial safety net. In 2026, many of the businesses that thrive are those that have successfully converted a portion of their expected monthly income into a “subscriber base,” effectively insuring themselves against the quiet weeks that traditionally break a small business’ back.

Working out what incentives you can offer clients in return for long-term support should be a priority for all small business owners. Your accountant can help you to both determine what incentives you would be able to offer over the long-term, as well as assist in determining the subscription prices for these services. Remember, cash flow and the ability to maintain these offerings are essential to the scheme’s success.

Marketing has also changed. Much of today’s most effective marketing isn’t happening on the algorithm, it’s happening on the sidewalk. “Neighbourhood stacking” is the practice of collaborative loyalty loops between physical neighbours. A local cafe, a boutique, and a bookstore create a closed-loop ecosystem where a purchase at one grants a specific, meaningful benefit at the others. This leverages what many call the “golden dome” of local trust.

This hyper-local synergy keeps consumer spending within the immediate community. Now, this trend is also expanding into service businesses, and through the freelancing community. For instance, a copywriter, designer and project manager may agree to offer a 15% discount on each other’s services in exchange for the initial hire of one of them.

By “stacking” their influence, small businesses create a combined value proposition that rivals the convenience and economies of scale of much larger companies. Most customers prefer to buy local – provided the price is right.

If you’re worried about the drain discounting will have on your bottom line, remember that these losses are more than mitigated by the fact that you’ve been able to reduce the cost of customer acquisition to near zero.

“A budget is telling your money where to go instead of wondering where it went.” (Dave Ramsey)

The unprecedented volatility of 2026 has brought about geopolitical disruption, volatile markets, rand weakness and rising input costs. This places real pressure on South African businesses of every size.

In addition, for businesses with international invoices, rand volatility can turn a profitable deal into a loss overnight if the rand weakens between order and payment, or the cost of goods skyrockets.

In this unpredictable economic climate, meaningful and closely monitored budgets are still the foundation on which sound business decisions are made.

Is my business achieving its targets? Where is my team underperforming? What if supplier costs increase by 10%? What happens if income drops by 5%? How to pivot?

Fundamentally important questions like these can all be answered by effective budgeting.

While their primary purpose is tracking and measuring income, expenditure and cashflow, effective budgets also deliver many other benefits. Having a budget to refer to makes scenario planning easier, helps you to optimise resources, and shows whether your resources and business goals are aligned. The bottom line? Budgeting encourages informed business decision-making and faster responses to market changes.

In volatile markets, budgeting is much more important than usual. Here are some tips for not only surviving the storm, but hopefully coming out of it in stronger shape.

A well-structured and regularly reviewed budget gives your business the clarity and agility to navigate disruption, manage shortfalls, and seize opportunity. It aligns your resources with your strategy, strengthens decision-making, and builds the financial resilience your business needs to weather ongoing uncertainty and emerge stronger.

![]()