Budget 2026: What it Means for You and Your Business

The 2026 Budget marks an important turning point for South Africa.” (Dr Duncan Pieterse, Director-General, National Treasury)

Some of the best news in Budget 2026 is the real GDP growth of an estimated 1.4% for 2025, rising to 2% in 2028, and a debt ratio that will stabilise during this financial year and decline thereafter.

Inflation also declined to 3.2% in 2025 (from 4.4% in 2024), improving affordability for households and keeping interest rates down. At the same time, growth-enhancing reforms have progressed and confidence in South Africa’s fiscal outlook has improved, enabling a sovereign ratings upgrade and lower borrowing costs.

No income tax or VAT increases

Against this backdrop, government has withdrawn the R20 billion tax increases it had planned for this budget and instead proposes inflationary relief for taxpayers.

This means no increase in VAT and no increase in income tax for individual or corporate taxpayers.

Inflationary relief, finally

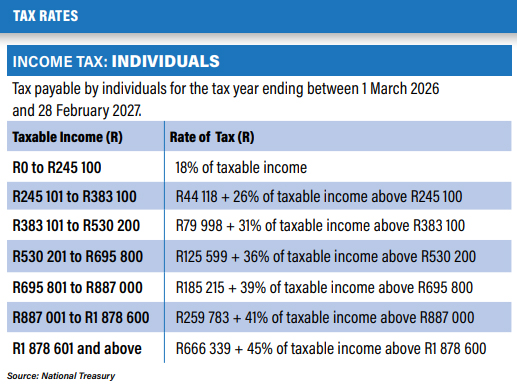

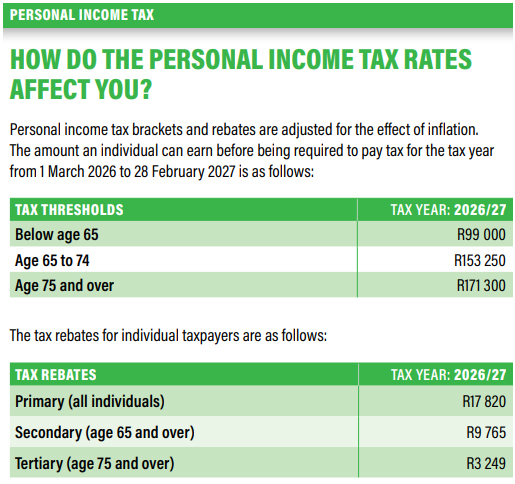

After two years with no inflationary relief, personal income tax brackets and medical tax credits are fully adjusted for inflation.

The tax threshold for individuals below age 65 is now R99 000, and medical tax credits will increase from R364 to R376 for the first two members, and from R246 to R254 for additional members.

Bottom line: taxpayers will keep more of their income in real terms than in the previous two years.

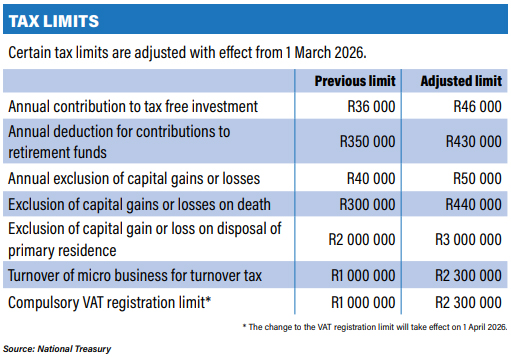

In addition, limits, rebates and duties are also inflation-adjusted for contributions to tax-free investments, the retirement funds deduction cap and capital gains tax (CGT) exclusions.

An increase in the annual tax-free savings account contribution limit to R46 000 (from R36 000) and the limit to retirement fund deductions from R350 000 to R430 000 are encouraging South Africans to save more.

Capital gains tax limits

The Budget also proposes increasing the annual exclusion on capital gains tax from R40 000 to R50 000 for individuals and special trusts, and the annual exclusion for individuals in the year of death from R300 000 to R440 000.

The exclusion that applies on the disposal of a primary residence will increase from R2 million to R3 million. Very good news for anyone planning on selling their home.

Corporate tax

The corporate tax rate remains unchanged at 27%. The global minimum tax rules will be implemented in 2026/27, a move expected to raise around R2 billion (down from an earlier estimate of R8 billion) by reducing profit shifting by multinationals.

More good news for businesses, especially small companies, is the increase in the VAT registration threshold to R2.3 million (previously R1 million), effective from 1 April 2026.

In addition, asset disposals by small businesses of as much as R15 million will be exempt from capital gains tax, a 50% increase on the current limit.

The annual turnover limit for turnover tax is also adjusted for inflation (from R1 million to R2.3 million). In addition, the restriction on tax year end dates will be removed to make the turnover tax regime more attractive.

A proposed review of the urban development zone tax incentive will explore better support for affordable housing developments in urban areas.

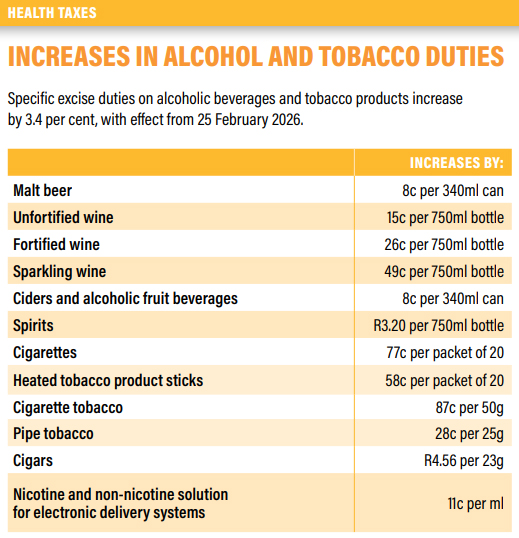

Sin taxes & fuel

Alcohol, tobacco, and vaping excise duties already increased in line with inflation (3.4%), effective 25 February.

Under consideration is a national online gambling tax, proposed at 20% on gross revenue, for further consultation during 2026.

The customs and excise levies on fuel remain unchanged but fuel levies have increased, with the general, Road Accident Fund and carbon tax levies up for both petrol and diesel from 1 April.

Other tax proposals

Local investors diversifying offshore will appreciate the increase in the single discretionary allowance (SDA) for individuals from R1 million to R2 million per calendar year.

The Budget also proposes that investment returns generated by regular collective investment schemes (CIS) and retail investment hedge funds be taxed as capital, to encourage savings and to provide the industry with tax certainty

Streamlining In-House Accounting Processes with AI

Artificial intelligence and generative AI may be the most important technology of any lifetime.” (Marc Benioff, CEO, Salesforce)

Traditional accounting involves a great deal of manual processing, endless menial tasks, and plenty of opportunities for mistakes and typos – all of which can mean long waiting periods for financial reports that are crucial for decision-making.

AI is changing this through advanced technologies like machine learning, natural language processing, generative AI, and intelligent automation. It can streamline accounting and finance processes, reduce human error, and empower you to make real-time data-driven decisions with greater certainty.

Many proactive businesses are already experiencing the benefits of integrating AI into their bookkeeping and accounting workflows.

Benefits of AI in accounting processes

- Faster processing: AI dramatically accelerates routine accounting tasks, like invoice processing and bank reconciliations. These previously tedious manual processes are now completed in minutes.

- Streamlined expense management: From a photo taken with a phone, AI can extract relevant information from receipts and other documents, categorise expenses according to company policy, and route claims for approval automatically. Reimbursements happen faster, and less time is spent chasing paperwork.

- Greater accuracy: While manual data entry inevitably leads to mistakes, AI systems achieve impressive accuracy rates. AI also consistently applies the correct rules to every transaction and maintains complete audit trails automatically. This means less time spent fixing errors, fewer penalties, and greater confidence in your financial reports.

- Cost savings: Reduced labour costs and fewer errors result in ongoing savings that multiply as your business grows.

- Scalability: Automated platforms can accommodate significant growth with minimal additional resources, supporting expansion without requiring corresponding overhead increases.

- Proactive problem-solving: AI can flag unusual patterns immediately and spot issues before they become problems, for example by predicting cash flow constraints before they occur.

- Real-time financial visibility: With AI you can say goodbye to the traditional monthly close process and hello to continuous accounting, where accounts remain perpetually up-to-date.

- Enhanced fraud protection: Machine learning algorithms can continuously monitor transactions for suspicious patterns, helping protect businesses from both external fraud and internal irregularities. AI can scan 100% of a company’s transactions to identify inconsistencies or potential fraud, replacing traditional manual sampling methods.

What AI means for your business

By embracing AI-driven tools, businesses can streamline financial operations, improve accuracy and decision-making, reduce costs and risks and gain a competitive edge in today’s digital economy.

If your current in-house processes still rely heavily on manual grunt work, it may be time to explore AI-enabled alternatives.

A good starting point would be to identify repetitive tasks like manual data entry or document chasing that delay your accounting processes. Start with one specific workflow: let’s say, Accounts Payable automation, training staff to shift from doing the work to reviewing the AI-generated outputs and managing any exceptions. Once you’ve got that waxed, you can start overhauling other processes.

Not a silver bullet

Experts widely agree that AI is extremely unlikely to replace accounting professionals, whether working in companies or in advisory firms. However, AI does offer great potential to transform accounting roles by automating routine tasks for enhanced efficiency and accuracy, and by enhancing analysis and decision-making capabilities.

Budget 2026: Your Tax Tables and Tax Calculator

Budget 2026 has brought long-overdue relief to taxpayers by not imposing VAT or income tax hikes and by adjusting the tables for tax rates, rebates and credits for inflation. Of course, some tax hikes were always going to happen: inflation-linked increases on sin taxes took effect on 25 February already and the fuel levies also increased.

This selection of official SARS Tax Tables and other useful resources will help clarify your tax position for the new tax year. Then follow the link to Fin 24’s Budget Calculator (just follow the four-step process) to do your own calculation.

Individuals taxpayers

Source: National Treasury

Source: National Treasury

Tax limits adjusted

Source: National Treasury

Sin taxes raised

Source: National Treasury

Fuel Levy hikes

Source: 2026 SARS Budget Guide

How much will you be paying in income, petrol and sin taxes?

Use Fin 24’s four-step Budget Calculator here to find out the monthly and annual impact on your income tax, as well as what you will pay in terms of fuel and sin taxes.