Business Hack: How to Better Define Your Target Market

“Defining your target market is about understanding motivations, challenges, and goals. Without this, your messaging falls flat and your marketing budget burns fast.” (Elena Kwan, Founder of MarketLens Consulting)

Fundamentally, businesses start because business owners believe they see a gap and aim to fill it. Their target market is built into the essence of the business. And yet, statistics show that at least one third of those business owners were wrong all along.

Many entrepreneurs think their product or service is for “everyone”, but trying to serve everyone usually means you end up serving no one well. Identifying and refining your real audience is critical to creating effective marketing campaigns, building better products, and sustaining long-term growth.

Here are five practical tips to help you better define and refine your target market.

1. Start with the problem you’re solving

As a business owner, the first thing you need to do is identify the specific problem your product or service addresses. Ask yourself: Who has this problem? Who is actively looking for a solution? The more precisely you can answer these questions, the closer you are to identifying your core market.

Once you understand the problem, look at existing customer data or run surveys to determine the people most likely to benefit from your solution. Don’t make assumptions. Focus on the why behind their purchasing decisions.

2. Build a customer persona (and revisit it often)

A customer persona is a semi-fictional profile of your ideal customer based on research, data, and interviews. Include details like age, job title, income, goals, frustrations, preferred social media platforms, and buying behaviours. Giving your customer a name and a story will help you recall the important aspects of the person you are serving.

But remember, a persona isn’t static. As you grow and collect more data, revisit and refine this profile. According to Sales For Startups, companies that use updated personas achieve 73% higher conversion rates than those that don’t.

3. Segment your audience

Not every customer will have the same needs or behaviours – and just because someone falls into your target market, doesn’t mean they are automatically going to buy from you. Audience segmentation allows you to create more tailored marketing strategies. Start with basic segments like age, location, or purchase behaviour. Then drill down into psychographics such as values, attitudes, and lifestyle.

For example, two people buying your eco-friendly cleaning product might do so for different reasons: one for health reasons, the other out of environmental concerns. Understanding these motivations enables you to craft more resonant messaging.

4. Use analytics to refine your focus

Data should drive your decisions. Use website analytics, social media insights, email open rates, and CRM (customer relationship management) data to understand who’s engaging with your content, who’s buying, and who isn’t. Look for patterns: Which landing pages convert best? Which demographic clicks through the most?

Your accountant can help you lift accurate sales data for different periods. This can be used to track the success or failure of special offers, product launches and other sales events to narrow down the areas that are working.

According to a survey by Salesforce, 76% of marketers say data-driven decision-making is crucial in campaign performance. By comparing your ideal audience to actual customer behaviour, you can adjust your messaging or target more profitable segments.

5. Actually talk to your customers

The most underrated source of insight is your customers themselves. Schedule interviews, send out surveys, or talk to users after a successful sale. Ask open-ended questions like:

- “Why did you choose us?”

- “What alternatives did you consider?”

- “What almost stopped you from buying?”

These conversations will undoubtedly uncover objections you hadn’t considered, new segments you didn’t plan for, or even product ideas for future growth. And remember: customers are often more honest in conversation than on email.

The bottom line

Defining and refining your target market isn’t a once-off job. It’s an ongoing process that evolves as your business, market conditions, and customer needs change. But investing the time upfront, and revisiting it regularly, can mean the difference between scattered sales and scalable success.

How Funding Budget 3.0 Will Impact You: Project AmaBillions

“We accept the responsibility to achieve the 2025/26 revenue estimate presented by the Finance Minister Mr Enoch Godongwana.” (SARS Commissioner Edward Kieswetter)

Removing the contentious proposed VAT increases from Budget 3.0 led to a shortfall in revenue that necessitated new revenue sources.

One of these is the inflation-linked fuel levy increases of 16c for petrol and 15c for diesel, which became effective on 4 June and will impact all individuals and entities in the country.

Another alternative revenue source is going to come from SARS’ upping its collection of outstanding tax debt – with Treasury expecting an additional R20 billion to R50 billion per year from intensified debt collection efforts.

The tax measures contained in Budget 3.0 will raise an additional R18bn in 2025/26. A further R20bn in as-yet-unknown tax measures are postponed to Budget 2026 – unless SARS collects an extra R35bn in outstanding taxes.

SARS has accepted the challenge and Budget 3.0 allocated a further R4 billion to SARS to fund the debt recovery. (In addition to the R3.5bn previously allocated to the cause.)

‘Project AmaBillions’?

In what the media refers to as “Project AmaBillions” and what SARS calls its “compliance programme”, an intensified effort will be made to collect a greater slice of the estimated R800 billion in unpaid taxes – the so-called “tax gap”.

SARS reported that just over R400 billion of the tax gap consists of undisputed uncollected debt. The rest is made up of a further R100 billion in debt currently under dispute, more than 54 million returns outstanding dating back several years, and 156,000 South Africans with substantial economic activity who are not registered taxpayers, or are not filing their tax returns. SARS says that it will focus on the undisputed debt, while accelerating work on collecting all debt by dutifully implementing its compliance programme.

In the last financial year SARS recruited and trained more than 800 new employees to collect debt, mainly via telephone calls and legal instruments. These efforts, says SARS, must result in a minimum collection of R20 billion.

To meet its revised revenue estimate this year, SARS is:

- Closing the tax gap, with a focus on undisputed debt.

- Broadening the tax base, targeting hard-to-tax sectors in the informal economy, particularly small enterprises and self-employed individuals.

- Using advanced data analytics and artificial intelligence to detect tax-compliance risks and improve overall compliance rates.

- Combating the illicit economy.

How does it affect me?

As SARS significantly steps up its revenue collection efforts, those eligible to pay tax – whether registered taxpayers or not – can expect less lenience and more SARS queries, verifications, audits and collection efforts.

In fact, the South African Institute of Chartered Accountants (SAICA) has been quoted in the media warning that the pressure on SARS to collect significantly more tax this year may result in “heavy-handedness” by SARS in its treatment of taxpayers.

SARS confirms that it upholds the rights of taxpayers to exercise their rights in law, which include among others, asking for payments to be deferred or paid in instalments, or to dispute the debt.

Taxpayers must also be wary of scams – the well-publicised increase in debt collection activity at SARS will be matched by an increase in financial scams by fraudsters pretending to be SARS employees or appointed debt collectors.

How we protect your interests

Even with SARS’ well-funded and intensified focus on compliance and debt collections, our specialist tax team will continue to ensure that your interests remain protected.

Our up-to-date tax expertise and best practices ensure you have clarity on your specific tax obligations, and that all these tax commitments are met accurately and timeously.

We can confirm the legitimacy of any SARS communications to protect you from scams and respond promptly and professionally to legitimate enquiries on your behalf. This includes swiftly rectifying any non-compliance issues, and handling demands for outstanding tax debts correctly.

We also monitor that SARS follows the correct legal processes – including adhering to timeframes and procedures in respect of assessments, refunds, dispute resolution, and instituting debt collection measures such as unauthorised bank account withdrawals – to ensure your taxpayer rights are respected.

The 2025 Tax Filing Season Opens on 7 July

“My sincere gratitude goes to the compliant taxpayers and traders who have continuously played their part in building our country. Ndza khenza.” (SARS Commissioner, Edward Kieswetter)

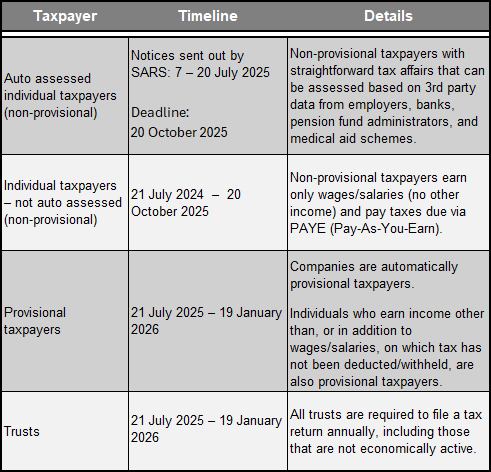

| Tax Filing Season 2025 officially opens on 7 July this year. This covers the 2024/2025 year of assessment: the period between 1 March 2024 and 28 February 2025.

During filing season, taxpayers complete and submit their tax returns, declaring their income and deductions to allow SARS to determine their final tax liability for the period under assessment. This year, for the first time, the majority of non-provisional taxpayers will be automatically assessed. Dates to diarise

Auto assessed? Here’s what to do…

Non-provisional taxpayers who are not auto assessed can start filing their tax returns from 21July 2025 until 20 October 2025. Provisional taxpayers (certain individual taxpayers and all companies) as well as trusts can start filing returns from 21July 2025 until 19 January 2026.

Fortunately, our team of seasoned tax professionals is ready to ensure you tick all these boxes. Let’s make this filing season an easy one! |