The 2026 Budget marks an important turning point for South Africa.” (Dr Duncan Pieterse, Director-General, National Treasury)

Some of the best news in Budget 2026 is the real GDP growth of an estimated 1.4% for 2025, rising to 2% in 2028, and a debt ratio that will stabilise during this financial year and decline thereafter.

Inflation also declined to 3.2% in 2025 (from 4.4% in 2024), improving affordability for households and keeping interest rates down. At the same time, growth-enhancing reforms have progressed and confidence in South Africa’s fiscal outlook has improved, enabling a sovereign ratings upgrade and lower borrowing costs.

No income tax or VAT increases

Against this backdrop, government has withdrawn the R20 billion tax increases it had planned for this budget and instead proposes inflationary relief for taxpayers.

This means no increase in VAT and no increase in income tax for individual or corporate taxpayers.

Inflationary relief, finally

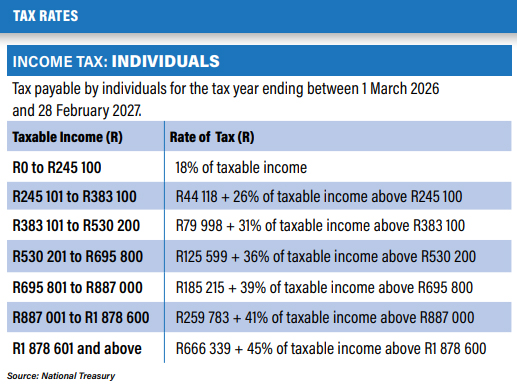

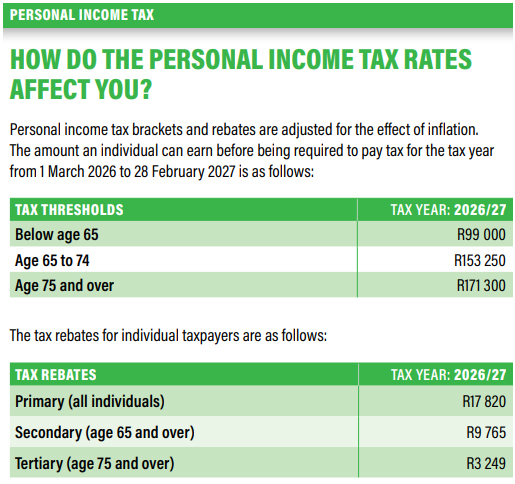

After two years with no inflationary relief, personal income tax brackets and medical tax credits are fully adjusted for inflation.

The tax threshold for individuals below age 65 is now R99 000, and medical tax credits will increase from R364 to R376 for the first two members, and from R246 to R254 for additional members.

Bottom line: taxpayers will keep more of their income in real terms than in the previous two years.

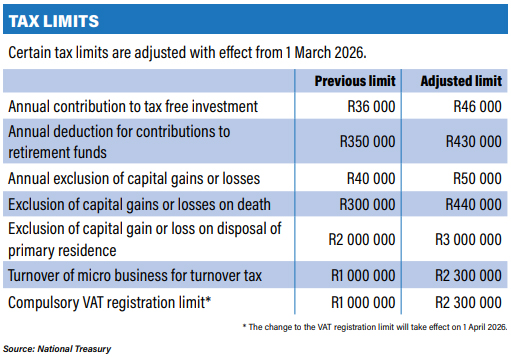

In addition, limits, rebates and duties are also inflation-adjusted for contributions to tax-free investments, the retirement funds deduction cap and capital gains tax (CGT) exclusions.

An increase in the annual tax-free savings account contribution limit to R46 000 (from R36 000) and the limit to retirement fund deductions from R350 000 to R430 000 are encouraging South Africans to save more.

Capital gains tax limits

The Budget also proposes increasing the annual exclusion on capital gains tax from R40 000 to R50 000 for individuals and special trusts, and the annual exclusion for individuals in the year of death from R300 000 to R440 000.

The exclusion that applies on the disposal of a primary residence will increase from R2 million to R3 million. Very good news for anyone planning on selling their home.

Corporate tax

The corporate tax rate remains unchanged at 27%. The global minimum tax rules will be implemented in 2026/27, a move expected to raise around R2 billion (down from an earlier estimate of R8 billion) by reducing profit shifting by multinationals.

More good news for businesses, especially small companies, is the increase in the VAT registration threshold to R2.3 million (previously R1 million), effective from 1 April 2026.

In addition, asset disposals by small businesses of as much as R15 million will be exempt from capital gains tax, a 50% increase on the current limit.

The annual turnover limit for turnover tax is also adjusted for inflation (from R1 million to R2.3 million). In addition, the restriction on tax year end dates will be removed to make the turnover tax regime more attractive.

A proposed review of the urban development zone tax incentive will explore better support for affordable housing developments in urban areas.

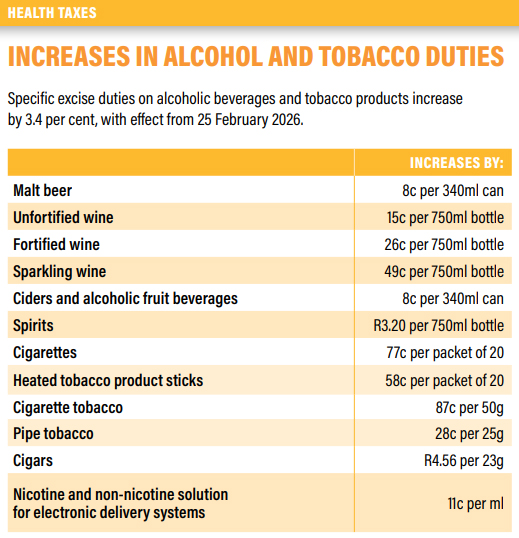

Sin taxes & fuel

Alcohol, tobacco, and vaping excise duties already increased in line with inflation (3.4%), effective 25 February.

Under consideration is a national online gambling tax, proposed at 20% on gross revenue, for further consultation during 2026.

The customs and excise levies on fuel remain unchanged but fuel levies have increased, with the general, Road Accident Fund and carbon tax levies up for both petrol and diesel from 1 April.

Other tax proposals

Local investors diversifying offshore will appreciate the increase in the single discretionary allowance (SDA) for individuals from R1 million to R2 million per calendar year.

The Budget also proposes that investment returns generated by regular collective investment schemes (CIS) and retail investment hedge funds be taxed as capital, to encourage savings and to provide the industry with tax certainty