Is Your Trust Registered and Ready for Income Tax?

“A trust is a ‘person’ for tax purposes and is therefore a taxpayer in its own right.” (SARS)

SARS recently sent out a reminder confirming that in terms of the Income Tax Act, 1962 (ITA), all trusts are taxpayers and that the trustees, who are also the representative taxpayers of the trust, have a responsibility to register the trusts – whether active or dormant – for income tax purposes.

The representative taxpayer (trustee/s), or the appointed tax practitioner, must also file an income tax return for the trust on an annual basis, and before the tax season deadlines to avoid penalties and interest.

Trusts that are required to register include all local trusts, non-resident trusts that are effectively managed in South Africa, as well as non-resident trusts that derive income from a South African source.

Why business owners use trusts

Trusts are used to hold, protect and ensure the continuity of ownership of personal or business assets, shares in businesses, and the right of use of assets.

The benefits include protection of assets against creditors, for example in the case of liquidation or sequestration, and against other parties – for example an ex-spouse, or ill-intentioned family member.

Where appropriate, a trust can be a useful tool to help ensure effective future planning; achieve continuity through efficient succession; and even managing certain tax liabilities, such as estate duty.

A business can also be registered in a business trust, also called a “trading trust,” instead of registering as a company with the CIPC. This option, however, is only appropriate where the main aim is conducting business, and a contractual agreement will task the trustees to manage the assets of the trust for a profit.

While a business trust can be useful to protect assets and safeguard the business owner against certain liabilities, it also has several drawbacks and may not always be the right alternative to registering a company.

Whether a business or personal trust, professional advice and guidance is crucial, because not only are the rules governing trusts complex, but the taxation of trusts requires specialised expertise.

The taxation of trusts

Whereas companies in South Africa are taxed at a flat rate of 27% for years of assessment ending after 31 March 2023, the income tax rate for trusts is currently 45%, and it is levied on any income retained in the trust.

This is the highest income tax rate, and trusts also do not qualify for any of the rebates provided for in Section 6 of the Income Tax Act.

Trustees may allocate income and capital to multiple beneficiaries, so that the tax obligation is spread, possibly at a lower rate in some instances. This is because, depending on circumstances, income distributed may be taxable in the hands of the founder, the beneficiaries or the trustees.

There are also special trusts, taxed at a sliding scale of 18% – 45% (the same as natural persons), and some special trusts also qualify for certain relief from Capital Gains Tax.

How to submit a tax return for your trust

It sounds quite simple in theory: an ITR12T must be completed and submitted.

In reality, a ITR12T trust tax return is a 31-page document, and completing it correctly is no quick or easy task.

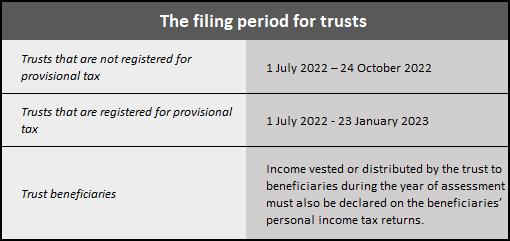

Firstly, a trust must be registered with SARS for the taxes for which it may be liable. In addition, the trustees of the trust – who are also the representative taxpayers of the trust – must file the return within the tax season deadline. This responsibility may be conferred to a specific trustee, or to a professional appointed by the trustee(s).

To make it easier to comply, SARS has announced some enhancements to its system. For example, whereas one could previously only register a trust via a visit to a SARS branch, taxpayers can now register a trust for tax purposes through the SARS Online Query System and also submit any supporting documents online.

Furthermore, the ITR12T trust return form is now available on eFiling. The representative of a registered trust can request the return on eFiling and customise it by completing the questions on the Tax Wizard. Requesting the ITR12T to be posted, as was previously required, is no longer an option and trust returns received via post will be rejected.

Taxpayers registered for eFiling are also able to complete and submit the return online. Only trusts with ten or fewer beneficiaries have the option to have the ITR12T return captured by a SARS agent at a branch, and only if an appointment has been made.

When the filing period for trusts ends, SARS will raise original estimated assessments on ITR12Ts that were not officially filed by the taxpayer.

After the estimated assessment has been raised by SARS, the taxpayer will be allowed to request an original (new) return to be submitted to SARS. The same estimated return will be issued on eFiling to be completed, with a new version number of the return.

The taxpayer will be able to request a correction after the original return has been submitted, until one or two rejection letters have been received from SARS. Thereafter, the taxpayer will have the option to dispute the decision taken by SARS.

Bear in mind…

- SARS introduced a number of form and system changes in respect of trusts from 24 June 2022.

- SARS has advised trusts that all outstanding income tax returns are submitted without delay to avoid further penalties and interest.

- SARS reminds trusts not registered for income tax purposes of the availability of the Voluntary Disclosure Programme (VDP), an option that should only be considered after obtaining professional advice.

- If the ITR12T return is not submitted by the relevant deadline, the trust will be liable for an administrative penalty due to non-compliance.

- Provisional taxpayers are required to make provisional tax payments within six months after the commencement of a year of assessment and then again by the end of the year of assessment.

- The trust is required to keep all the relevant material and supporting documents for a period of five (5) years from the date of submission of the return. SARS may, within the 5-year period, request these documents to verify the information that was declared on the ITR12T.

Top Ten Tips for Maintaining a Strong Cash Flow

“Never take your eyes off the cash flow because it’s the lifeblood of business.” (Sir Richard Branson)

Managing cash flow is often one of the biggest challenges business owners face and is also the reason for a concerningly large percentage of business failures.

Cash flow can be defined as the total amount of money that comes in and then goes out of a business and – crucially – the timing between cash flowing in and cash flowing out.

A positive cash flow means the business earns more than it spends and is a key indicator of the financial health of your business. A consistent, positive cash flow ensures there is cash on hand to cover payroll, expenses and loan repayments on time and enables business growth by ensuring cash is available for timely equipment purchases and upgrades, and investment in new opportunities that arise.

As such, proper cash flow management is key to your short – and long-term financial success, and cash flow strategies should be a priority in your business planning. Good cash flow planning will allow you to predict when money can be expected to be received, and when it must be paid out. With this information, you can plan ahead and make smart business decisions.

Implementing the ten top tips below for maintaining a strong cash flow will ensure businesses can enjoy all these benefits in a short time and with little effort.

- Increase sales – More sales are obviously the preferred strategy for a business to grow the amount of cash flowing into the business, and it provides more benefits than other options such as liquidating assets or taking out a loan.

- Collect client payments quickly – Late payments from clients are one of the most common reasons why businesses experience cash flow problems. Manage this proactively by invoicing clients promptly and sending monthly statements early. Verify the invoice was received, and contact late payers well in advance, reminding them to pay on time. Follow up on late payments right away, offer discounts to clients who pay early, and implement a cash-on-delivery policy for chronic late-payers.

You could also consider requesting deposits when taking orders, and if you offer credit to clients, make sure to do credit checks first and maintain stringent credit policies.

- Adjust inventory – Inventory that doesn’t sell well will also negatively impact your cash flow. Move outdated inventory and offload less frequently purchased items for discounted prices and don’t replace this stock – rather invest more into stocking items that do sell well.

- Manage and trim expenses – Cash flow reduces as and when expenses are paid, so managing your expenses better and eliminating unnecessary costs will immediately boost cash flow. Also consider other ways to conserve cash flow, such as leasing instead of buying equipment.

- Prioritise payments – Know exactly which payments must be made when, then order according to priority, and spread payment dates so the most important bills are paid first and the less critical account payments with more flexible payment dates are paid later. Where necessary, negotiate payment terms with your suppliers.

- Increase efficiencies – Take advantage of technological advances and artificial intelligence-enabled solutions, such as apps, software and equipment to streamline your business processes and increase efficiency. Also, consider identifying operations or tasks that can be cost-effectively outsourced to freelancers and third-party service providers.

- Use a business credit card – A well-managed business credit card could be used to pay day-to-day expenses during the month to free up cash. This will require keeping a tight record of those expenses and being disciplined in repaying the full balance within the interest-free period. It will also allow the business to benefit from any rewards programs that can reduce expenses, such as a certain percentage of cash back on some purchases.

- Keep a line of credit – A business line of credit can be a saving grace for small businesses and companies impacted by seasonality. It provides quick access to funds when needed, for example, to bridge gaps between invoicing and payment, to buy equipment, to cover seasonal or unexpected expenses, or to take advantage of growth opportunities. The business will have to negotiate such a facility before cash flow problems arise.

- Make your money work – At times, there may be a surplus of cash, for example, in seasonal businesses, and at these times, it is crucial to make sure this money works for the business. This can be achieved through building up a reserve fund for emergencies, which experts suggest should ideally be sufficient to cover six months of business expenses; making smart short-term investments and paying off debts faster to reduce interest and shorten loan terms. Consider investing any surplus cash, short-term or otherwise, in a money-market call account to earn interest rather than leaving it idly resting in the bank account.

- Use accounting expertise – Successfully monitoring and projecting cash flow often requires professional assistance. Alongside the balance sheet and income statement, the crucial cash flow statement is one of the three main types of financial statements. Generally covering three main areas: everyday business operations, investment activities, and financing, it reveals trends and allows potential cash flow problems to be identified and managed in time.

Projecting future cash flow requires assessing the previous year’s numbers as the basis of cash flow for the following year and then adjusting these numbers for anticipated changes, such as new pricing, more staff and new funding sources. Of course, these forecasts will change continuously, so it’s important to monitor cash flow on an ongoing basis.

Speak to your accountant about accessing cash flow reports regularly and for professional assistance in understanding what they reveal about your business, to enable more accurate and relevant business decisions.

Your Tax Deadlines for July 2022

- 7 July – Monthly Pay-As-You-Earn (PAYE) submissions and payments

- 25 July – Value-Added Tax (VAT) manual submissions and payments

- 28 July – Excise Duty payments

- 29 July – Value-Added Tax (VAT) electronic submissions and payments & CIT Provisional payments where applicable.