How To Avoid Bad Customers

“Happy customers are your biggest advocates and can become your most successful sales team.” (Lisa Masiello)

Anyone who has started a business has had those meetings. The ones where you trade a dozen emails explaining what you do and how you do it, what your rates are and why you are the best, and now your potential client has asked for a meeting. You drive to the other side of town, have a two-hour meeting explaining all the things you had explained before, and get back to the office feeling like you did everything you could, and then you wait. Perhaps for weeks there is no response from the prospect and you wonder exactly where you may have gone wrong. The problem here might not be you, but may instead lie with the potential customer, and all that time and effort you sunk into trying to win their business was perhaps always going to be wasted.

Success for a small to medium business is built on resource management. Those companies that manage to get the most return on investment are the ones that will grow the fastest and last the longest. Getting this return requires not only that you create excellent products or deliver excellent services, but that you do this with the right people – and that includes your customers. Being able to tell the difference between good customers and bad ones is a skill no one starts with, but everyone can learn. Here is a guide to recognizing a bad client before you get too committed.

Recognise what makes a good client

Being able to tell the difference between good clients and bad clients will first require you to know exactly what makes a good client. At a very basic level a good client is one that doesn’t take much of your time but is profitable. The best ones are regular customers as well.

Using your accounting software, you will very quickly be able to see which of your clients are giving you the most return for the effort being put in. While some clients you think of as “good clients” because they always take you to lunch or invite you to company golf days may not be having as much impact as you thought, the numbers will never lie.

Try to see if there are any patterns in the clients that deliver the most value to you. Are they of a particular size? Do they come from the same industry or are they from the same areas? What is it about your service or product that seems to appeal to those kinds of businesses? What are you doing for them that your competition can’t? Are there any other companies like them?

Now try to see if there are any patterns among the personalities who work for those clients and who pay for your services. What positions do they hold and do they have the power to sign purchase orders themselves or must they go further up the chain? Knowing these things will help you to avoid dealing with people who may not have the power at the end of the day to order from you and you might be better served focusing on those who can.

The first impression

In order to find good clients or customers, it’s important that your first meetings with them be as much about you examining them as it is about you selling yourself. Do not be afraid to ask the critical questions of them to gauge how much effort it’s going to take to get your first payment.

Are they simply weighing up options or do they have a project that needs completion by a certain deadline? Why are they looking for a new supplier or service? What happened to the people who used to do it? Clients who bad-mouth the previous company they worked with clearly had an acrimonious relationship and it may be time to ask yourself why.

While they may prove valuable in the long run, clients who are simply looking at options are going to be a lot more work moving forward. You may be called upon to offer advice, or chat over coffee more than you would like, and at the end of the day, the work that earns you money may never arrive. Those with project specifics and needs, on the other hand, are looking for solutions that you can provide and want to be quoted. At the end of the day they have to deliver a completed project and will need your help. These customers are much more likely to not only earn you money now but are clearly actually doing things rather than talking about them, making them far more likely to offer you work in the future too.

But even those with work that needs to be done immediately can come with warning signs. Any small business owner should automatically be aware of the clients who want you to “prove yourself” or “do a test job for free.” Filling your time with discount seekers ultimately means you can’t take on work for those companies that would actually want to pay you and anyone who asks you for free or heavily discounted first jobs may not value you or your time and should perhaps go immediately onto the bad customer pile.

This is a good time to also be cautious of those who refuse to work with a written contract. Anyone who actively does not want to sign on the dotted line likely has a very good reason for avoiding commitment and usually, that reason is that they don’t want to pay what or when they say they will. Remember that although in our law most verbal contracts are binding, only by reducing your agreement to writing can you minimise the risks of misunderstanding and dispute. If you insist on a contract and they suggest you don’t need one, rather walk away.

Watch out for red flags in the first few weeks

You are through the initial introductions, have quoted for work and after negotiation have had your quote accepted, in writing. Now it’s time to buckle down and do the job. This might feel like the time when you just want to focus on delivering the best work you can, but it’s also a time to be wary. Watch the client’s behaviour carefully over this period because it’s at this stage that the first signs of an imminent bad relationship will start to raise their heads.

Does the customer respect your time or do they want you to be available 24/7? Are they calling you after hours, or looking for constant updates on your work? Are their deadlines reasonable or does everything need to be done yesterday? Do they micromanage you or nit-pick your work? People with high demands aren’t always problematic, but when it crosses over into your personal time, and they think nothing of calling you late at night to hash out tiny details then you know they are already becoming more effort than they are worth.

You should be equally cautious of those clients who work the other way around as well. These clients who don’t respond to your emails or take weeks to get you answers to important questions. Clients who can’t be bothered to live up to their own project timelines will also struggle to meet your payment deadlines.

The third thing to look out for is those clients who are constantly adjusting the scope of the project. Scope creep starts out with asking you for a few small unpaid favours and slowly slips into the entire project taking on a different life to what was negotiated. Clients like this are usually more disorganised or inexperienced than dishonest but as the project grows and expectations around your workload increase, so should your remuneration. Don’t be afraid to speak up and ask for an adjustment to the contract.

The final red flag is if clients come back to renegotiate your rates for a job that’s already begun. Negotiating up front is normal and healthy, but when they don’t want to accept what has already been agreed or want to fiddle with the details it’s time to reconsider. This renegotiation technique is a sure sign they can’t really afford the project and at the end of the day they’re going to be someone who is likely to leave you unpaid.

At any stage…

So far all the issues that have arisen are probably excusable or can be overcome if the compensation is good enough, but there are some signs that are just too dangerous to ignore. If any customer of yours ever does any of these things it is far better for the long-term survival of your company to immediately terminate any further partnerships or projects and rapidly move on.

The first of these is when they ask you to copy brand logos, ideas or products from a competitor. Anyone willing to ask this of you neither respects you nor your company and certainly does not respect their competition. Being dragged into tacky business projects such as this will only end in your company being made to look bad as when they are inevitably caught, they will pass the blame squarely on to you and your new brand.

This warning goes double for any client who asks you to ignore the law or break it outright. Examples can range from the small, such as when you are in construction and they ask you to just go a little outside of the building code to the large, such as when they ask for kickbacks or offer incentives to work with specific companies. Any form of corruption or criminality will eventually not only ruin your company but could also ruin your life.

If you have been in business for any small amount of time you are bound to have come across some people who tick some of these boxes and might be reliving the trauma of projects you would rather forget. Now is the time perhaps to head over to “Clients from hell” for a wry laugh from these people who may just have had it a little worse than you.

Recession on the Horizon: Here’s How to Survive

“During recession greed dies, frugality survives.” (Amit Kalantri, Wealth of Words)

With yet another return of loadshedding in August, and major banks upgrading their forecasts to reflect an increased possibility of further economic downturns, recession feels inevitable in South Africa. A recession is simply where an economy stops growing and starts retracting. A generally held definition of recession is when the Gross Domestic Product of a country declines for two consecutive quarters, or half a year. Apart from the shrinking GDP, recessions typically come with reduced employment opportunities and incomes, and a stalling in industrial productivity, all of which then impacts all other aspects of life from retail sales to reduced travel and entertainment. To be overly simplistic, when people are scared about their futures, they stop spending, which in turn means businesses, particularly those relying on consumer spending, stop making as much money and the economy has nowhere to go but down.

Businesses, already on the edge from years of pandemic, are preparing themselves to take yet another battering. Managing these economically turbulent times has become an ongoing challenge. Fortunately, though we have had numerous recessions before, and unlike the pandemic, economists are better able to predict the beginning, if not the length of recessions. We also have evidence for the things you can do to make sure these economic downturns don’t close your business.

|

Loadshedding: Tax Incentives for Energy Efficiency and Alternative Power

“This is a call for all South Africans to be part of the solution; to contribute in whatever way they can to ending energy scarcity in South Africa.” (President Cyril Ramaphosa)

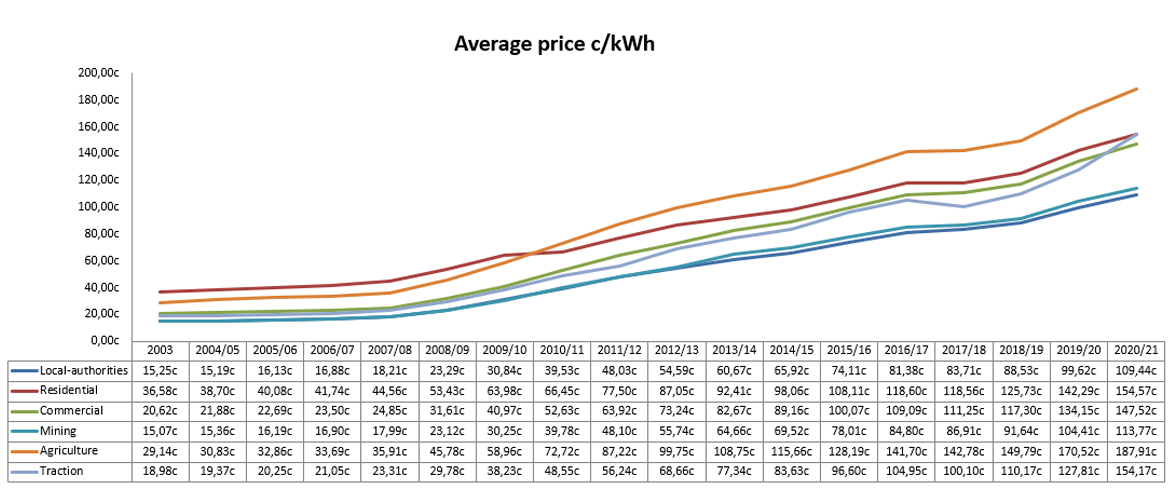

For more than a decade, local businesses have faced the huge challenge of an unreliable power supply from a state-owned monopoly that allowed very little in terms of affordable or practical alternatives.

In addition, since then Eskom’s electricity prices continued to skyrocket – increasing by more than 400%.

Click here to view | Source: Eskom Distribution

Just a month ago, Eskom proposed a further tariff increase of 32.7% to the National Energy Regulator of South Africa (Nersa) and is also contesting, in court, the tariff increase of 9.6% for 2022/23 Nersa allowed, which was far below the 20.5% requested.

A national crisis

South Africa’s energy crisis has been described as the biggest risk to the country’s economy. Recently President Cyril Ramaphosa, in his address to the nation on the energy crisis, announced measures to tackle it, including scrapping the licensing threshold of 100MW, Eskom buying more electricity from existing independent power producers, importing power from Botswana and Zambia, and doubling the amount of renewable generation capacity procured through Bid Window 6.

Of particular interest to businesses and individuals are the measures designed to enable businesses and households to invest in rooftop solar.

“South Africa has great abundance of sun which we should use to generate electricity. There is significant potential for households and businesses to install rooftop solar and connect this power to the grid,” the President explained. “To incentivise greater uptake of rooftop solar, Eskom will develop rules and a pricing structure – known as a feed-in tariff – for all commercial and residential installations on its network. This means that those who can and have installed solar panels in their homes or businesses will be able to sell surplus power they don’t need to Eskom.”

This certainly provides reasons for companies to re-assess the long-term viability of alternative energy sources, particularly photovoltaic (PV) solar energy projects, which are incentivised because of their low impact on the environment and our scarce water resources.

In particular, the President called on businesses to:

- seize the opportunities that have been created and invest in generation projects

- reduce consumption through greater energy efficiency.

The good news is that there are tax incentives to assist in achieving these national priorities.

Section 12B of the Income Tax Act provides for capital expenditure deductions for assets used in the production of renewable energy and particularly incentivises the development of smaller solar PV energy projects with an accelerated capital allowance of 100% in the first year for solar PV energy of less than 1MW.

Section 12U of the Income Tax Act provides for capital allowances for roads and fencing used in the generation of electricity.

Section 12L of the Income Tax Act is aimed at directly incentivising investments in local energy efficiency projects and provides a deduction for actual savings resulting from a reduction in energy use.

Capital expenditure deductions (S.12B)

Section 12B provides for a 50%/30%/20% income tax deduction over three years for certain machinery or plant – which means 50% of the costs of the assets can be deducted in year one, 30% in year 2, and 20% in year 3. These assets must be owned by the taxpayer, brought into use for the first time by the taxpayer, for the generation of electricity from, amongst others, photovoltaic solar energy or concentrated solar energy. The tax deduction also applies to any improvements to the qualifying plant or machinery that are not repairs related.

The following types of renewable generation projects may benefit from the allowance:

- wind power;

- photovoltaic solar energy;

- concentrated solar energy;

- hydropower (producing less than 30 megawatts); and

- biomass comprising organic wastes, landfill gas or plant material.

In respect of photovoltaic solar energy of less than one megawatt, a 100% income tax deduction is allowed in the first year of use.

What this means is that the cost related to a new solar power system can be deducted as a depreciation expense– reducing the income tax liability. The reduction can be carried over to the next financial year as a deferred tax asset.

In a previous binding ruling, SARS confirmed it will allow for both the capital cost of solar power units, as well as the direct cost of installation or the erection thereof.

The capital costs that may be deducted are:

- Photovoltaic solar panels;

- AC inverters;

- DC combiner boxes;

- Racking; and

- Cables and wiring.

In addition, related allowable costs of installation are:

- Installation planning expenses;

- Panels delivery costs;

- Installation expenses; and

- Installation safety officer costs.

Taxpayers installing assets used in the production of renewable energy, and particularly smaller solar PV energy projects or systems should investigate the tax benefits of Section 12B, particularly now that selling electricity back to Eskom will soon be a reality.

Capital allowances for roads and fencing (S.12U)

Section 12U provides for capital allowances for roads and fencing used in the generation of electricity greater than 5MW from wind; solar; biomass comprising organic wastes, landfill gas or plant material; and hydropower to produce more than 30MW. It is granted in full in the year of expenditure and covers improvements to the roads and fencing related to the generation project, as well as foundations or supporting structures.

Energy-efficiency incentive (S.12L)

Section 12L, read with the Regulations, allows any person or entity registered with the South African National Energy Development Institute (SANEDI) to claim a deduction for energy-efficiency savings derived from activities performed in the carrying on of any trade.

The incentive allows for a tax deduction for all energy carriers (not just electricity, but also fuel) but with the exception of renewable energy sources.

Ownership of energy-efficient machinery and equipment is not a requirement to claim a deduction under section 12L, so a lessee of the machinery or equipment can equally claim a deduction under section 12L.

The deduction is calculated at 95 cents per kilowatt hour or kilowatt hour equivalent of energy-efficiency savings and can create or increase an assessed loss.

A taxpayer must comply with certain requirements before being eligible for this deduction, for example, taxpayers are required to register with SANEDI, and a measurement and verification professional belonging to an accredited measurement and verification body must be appointed. An energy-efficiency performance certificate must be obtained from SANEDI detailing the energy-efficiency savings generated for the year of assessment.

Examples of energy-saving measures include, for example, investing in more efficient technologies such as LED lighting; installing clear acrylic door refrigeration equipment to reduce energy consumption in retail stores; using recycled waste heat from refrigeration plants or furnaces to reduce another electrical heating load; or investing in energy saving solutions for HVAC and refrigeration.

With this incentive, businesses can ensure their energy efficiency measures not only result in lower energy costs but also reduces their tax liability.

When heeding the President’s call to invest in generation projects and reduce consumption through greater energy efficiency, businesses and individuals are well advised to investigate further the tax incentives and rebates available. These are complex, so seek professional advice!