Your Tax Deadlines for April 2026

- 01 April: Start of the 2026/27 Financial Year

- 07 April: PAYE submissions and payments

- 24 April: VAT manual submissions and payments

- 29 April: Excise duty payments

- 30 April:

- VAT electronic submissions and payments

- CIT Provisional Tax payments where applicable.

15% Global Minimum Tax (GMT) Goes Live at SARS

“An agreement that will really change the world.” (Olaf Scholz, former German Finance Minister)

| In October 2021, a global minimum tax framework for large multinational enterprises (MNEs) was established with the introduction of the GloBE (Global Anti-Base Erosion) model rules by the OECD (Organisation for Economic Cooperation and Development).

These rules address profit shifting by multinational groups to low- or no-tax jurisdictions and ensure a minimum level of tax is paid on income in every jurisdiction in which MNEs operate. South Africa enacted the GloBE minimum tax legislation in 2024 and 2025, enabling SARS to impose a multinational top-up tax at a rate of 15% on the excess profits of affected MNE Groups. This tax effectively brings the overall taxation of foreign profits up to a minimum agreed level of 15%, where those profits have been subject to little or no tax offshore. As such, the GMT is expected to generate significant additional tax revenues by curbing tax avoidance, ensuring multinational corporations contribute their fair share of taxes, and extending the country’s tax base. The GMT is expected to raise an estimated R2 billion in South African tax revenues. The broadened tax base will open opportunities to lower the personal income tax burden on individuals, or to consider more globally competitive corporate tax rates than the current 27%, which is well above the international average. Which companies are directly affected?

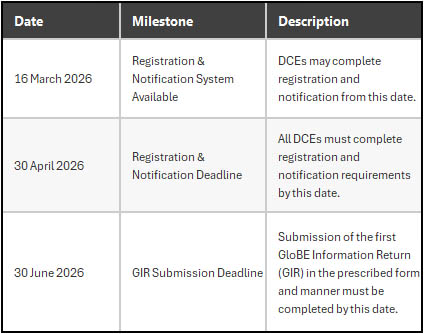

The GloBE Rules apply to MNE Groups whose consolidated annual revenues equal or exceed EUR 750 million in at least two of the tax years immediately preceding the reporting fiscal year. GMT deadlinesThe local legislation governing GMT is deemed to have come into operation on 1 January 2024 and applies to MNEs’ subsequent “fiscal years”. Here are the deadline dates as published by SARS.

Source: SARS How will the tax be calculated?

Registration and reporting obligations

SARS is ready: Are you?SARS is actively preparing to administer the GloBE framework, with a dedicated project team, including IT and system engineers, and a specialised unit within its Large Business & International Unit. It aims to promote voluntary compliance and simplify adherence with the GMT legislation. Even so, a significant compliance burden and increased reporting scrutiny awaits affected companies. They will have to comply with new and technically demanding rules, even if no global minimum tax is ultimately payable. This will likely require specialist expertise, resulting in substantial additional compliance costs. |

New VAT Thresholds: Thinking of Deregistering?

“Renette Oosthuizen, small business owner from Gauteng, had this tip: ‘Minister Godongwana, please increase the VAT registration threshold for small businesses to R2 million. The R1 million threshold has not kept pace with the cost of doing business.’” (Budget Speech 2026)

Some of the best news in the 2026 Budget is the proposed increases in the compulsory VAT registration threshold from R1 million to R2.3 million and in the voluntary registration threshold from R50,000 to R120,000, with effect from 1 April 2026.

This will immediately ease the disproportionate administrative burden and compliance cost on small businesses which would have had to register soon. What’s more, VAT registered businesses may apply to deregister for VAT if they no longer exceed the increased compulsory registration threshold on 1 April 2026.

Deregistering for VAT can improve cash flow. But it’s a decision that should not be taken without consulting us, as it can trigger substantial adverse tax consequences that might well convince you not to deregister.

Reduced admin and costs

The compulsory registration threshold had not been adjusted for inflation since 2009. The new R2.3 million threshold, which slightly outstrips inflation, will ease the previously disproportionate compliance burden relative to turnover on smaller businesses. It may also spur unrestrained growth among many small businesses which felt forced to contain themselves to avoid the VAT net and its never-ending impact on admin and cashflow.

Option to deregister

Given the above, many small businesses will be keen to deregister for VAT. The good news is that it is possible for VAT registration to be cancelled – provided certain requirements are met. The first is that all outstanding liabilities and obligations in terms of the VAT Act have been resolved or settled.

The Commissioner will issue a notice of cancellation of registration which will also inform the vendor of the date on which the cancellation takes effect and the final VAT period.

SARS says output VAT on certain assets on hand at the time must also be declared together with any other output tax and input tax in the VAT return for that final tax period. In other words, you must declare the amount of output VAT on the value of the business’ assets at the date of deregistration and pay this over to SARS.

There is also a general unpaid-creditor claw-back provision that requires a vendor to reverse previously claimed input VAT by accounting for output VAT on amounts due to creditors but not paid within 12 months of the date they became payable. This rule applies throughout the VAT registration period but is also triggered immediately before a vendor ceases to be registered.

Commonly referred to as “exit VAT”, this can cause immediate and possibly substantial financial implications that could strain your cashflow.

Before deregistering

If you are interested in deregistering for VAT, we urge you to speak to us to ensure you fully understand the financial implications and can carefully plan the timing to avoid tax surprises and cash flow problems.