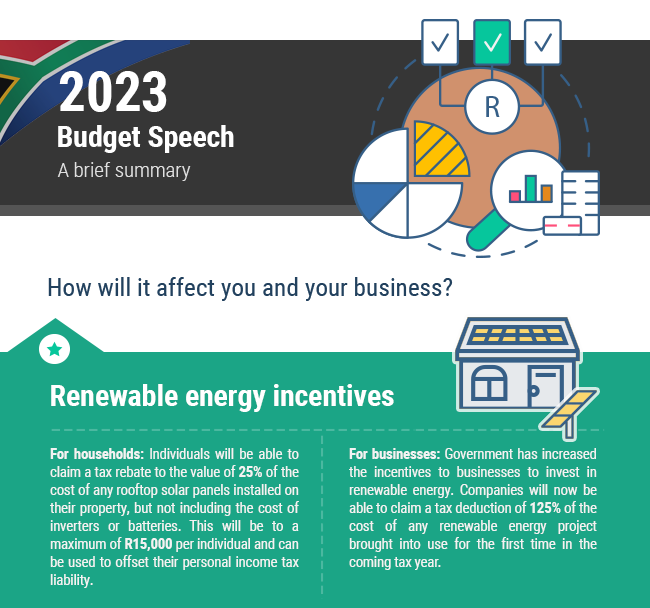

Budget Speech 2023 | How it affects you and your business

The 2023 budget speech delivered by Finance Minister Enoch Godongwana brought a fair amount of good news for South Africans.

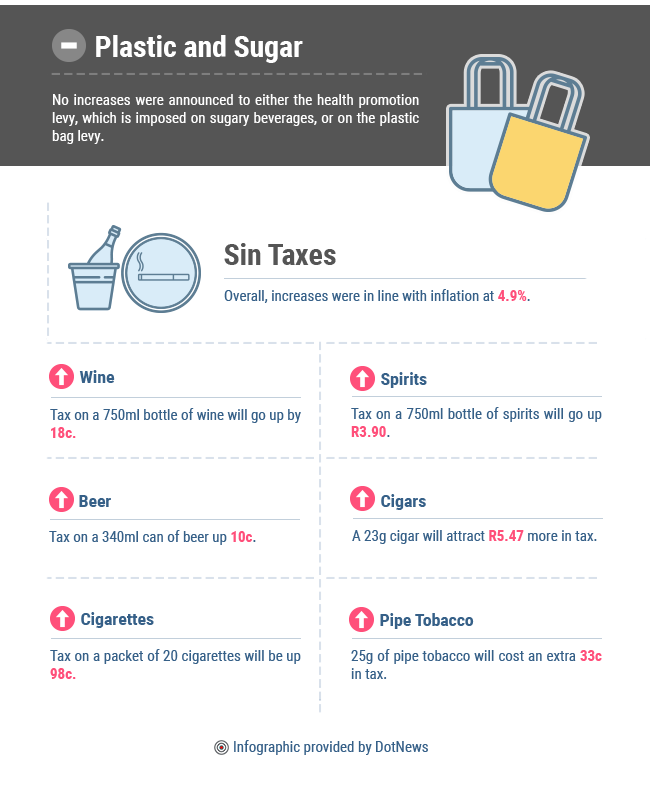

There will be support for households and businesses installing renewable energy, no income tax increases were announced, and the fuel levy remains unchanged, taking some pressure off people’s budgets.

However, the Minister could not avoid acknowledging that the problems at Eskom are a big challenge to the country’s growth prospects.

“The lack of reliable electricity supply is the biggest economic constraint,” Godongwana said.

He therefore announced that government would be taking over a big portion of Eskom’s debt to take some pressure off the utility, and that a number of steps were being taken to restructure the local electricity industry.

“Establishing a competitive electricity market will enable South Africa to ensure a stable, uninterrupted power supply as it transitions to a clean energy future,” National Treasury stated in its budget review.

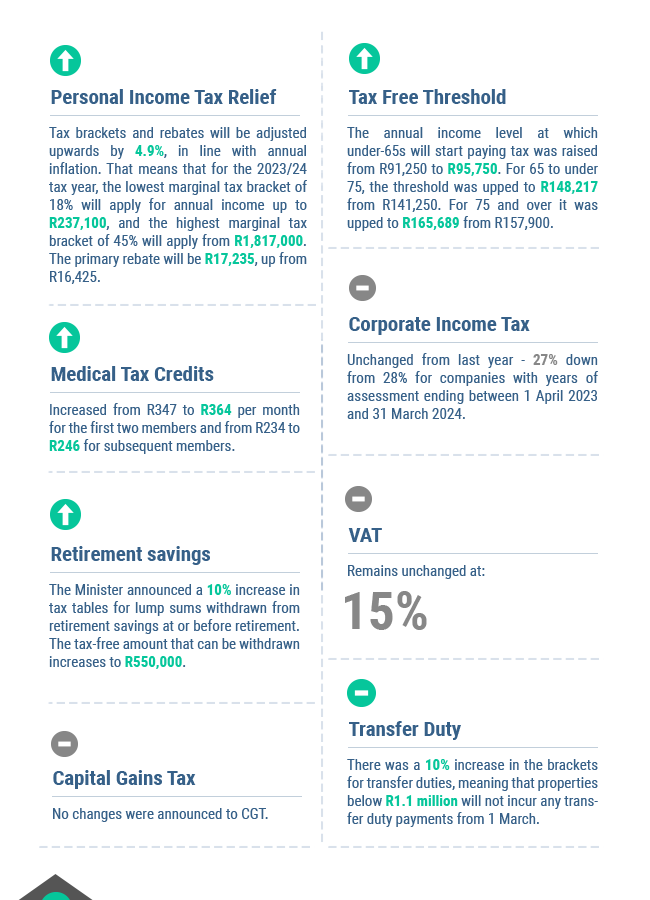

|

|||||||||||||||||||||||

|

|||||||||||||||||||||||

|

|||||||||||||||||||||||

Your Tax Deadlines for February 2023

- 7 February – Monthly Pay-As-You-Earn (PAYE) submissions and payments

- 27 February – Excise Duty payments

- 28 February – Value-Added Tax (VAT) electronic submissions and payments & CIT Provisional payments where applicable.

Loadshedding: Survival Tips for Small Businesses

“We want to assure business that by the time you get back to work in January, we will have a much more stable situation.” (Public Enterprises Minister, Pravin Gordhan, December 7, 2018)

With loadshedding now a constant reality in our lives and Eskom and the government offering no signs of any form of short-term recovery, small business owners are being forced to increasingly adapt in order to survive. Here are our top five tips that might help, beyond simply “buy a generator/inverter”.

Adopt work from home

Those who are single will have heard the advice to date someone on a different loadshedding schedule, and this tip can be liberally applied across a company. By allowing staff to work from home, most businesses can be reasonably assured of having someone online and capable of handling client calls and enquiries at any given time.

At the very least companies need to be looking at offering flexible work hours, so they don’t find employees sitting in the traffic caused by all the traffic lights being out, only to arrive at work to sit in the dark. Allowing staff to do the work when and where they want could do wonders for productivity. Perhaps you can even negotiate with a local coffee shop for discounts when your staff come to work there?

Move to cloud-based solutions

If you aren’t already using cloud-based solutions now is the time to adapt. Storing everything you do on the cloud with storage and backup solutions such as Dropbox or Microsoft’s OneDrive will mean your data can be accessed from anywhere and is much less likely to be lost should servers or computers become damaged by the power cuts. Set computers to do regular saves and backups so nothing gets lost.

Use mains-free tools

If your tools can come in a battery-operated version, then now is the time to start trading out of plug reliant technology. PCs should be traded in for laptops, electric cookers and fridges can be traded in for gas and everything from power tools to hairdryers have battery operated versions. Move your company’s main number to a cell phone or to a VoIP solution and make sure all key personnel cell phones are permanently charged.

Unplug equipment

The second the power goes down it’s time to unplug all the expensive equipment. Don’t take the risk of the surge destroying your vital machines, assembly lines and computers when the power comes back on. If you can, invest in insurance, but make 100% sure that it covers loadshedding damage, as some companies have removed that protection from their contracts.

Ensure that your, and your key employees’ Wi-Fi connections are attached to a UPS system.

Use more than one payment system

Using two or even three different network options will ensure you are always able to take payments whenever your equipment is charged, even if the power is off. Don’t lose a vital sale or shut up shop simply because you have a contract with one network service provider whose tower always goes down when the power is off.

And of course, get solar, install an inverter and/or buy a generator – there are tax incentives for some solutions that your accountant can help you with.