Your Tax Deadlines for March 2023

- 7 March – Monthly Pay-As-You-Earn (PAYE) submissions and payments

- 30 March – Excise Duty payments

- 31 March – End of the 2022/23 Financial Year

- 31 March – Value-Added Tax (VAT) electronic submissions and payments & CIT Provisional payments where applicable.

Budget 2023: Your Tax Tables and Tax Calculator

The big Budget Speech 2023 tax news was the introduction of tax incentives for investing in rooftop solar and renewable energy. The Budget also detailed tax relief in the form of adjusted tables for tax and rebates for individual taxpayers, adjusted tables for retirement tax and transfer duty, and the expected increases in ‘sin’ taxes. How will these changes affect you directly?

To better understand the impact of the Budget on you and your business, here is a selection of official SARS Tax Tables, then follow the link to Fin 24’s Budget Calculator to do your own calculation.

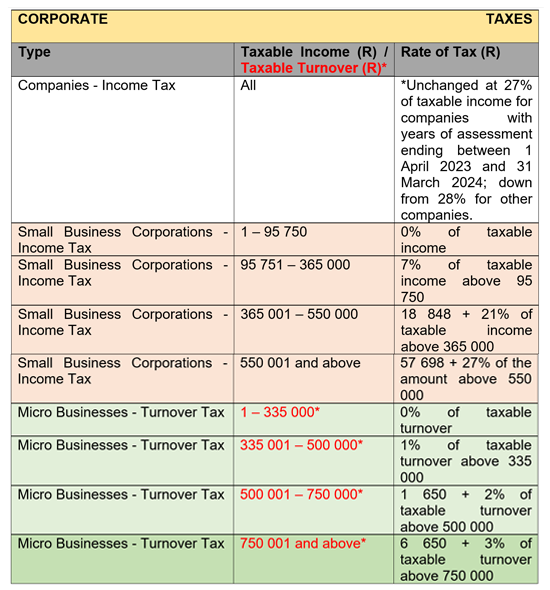

Businesses – corporate tax rates unchanged*

Source: SARS’ Budget Tax Guide 2023

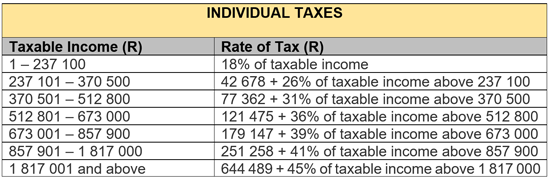

Individual taxpayers – tax tables adjusted

Source: SARS

Source: SARS

Source: SARS

Transfer duty table – adjusted

![]()

Source: Budget 2023 People’s Guide

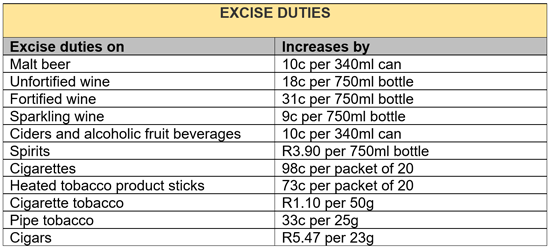

Sin taxes raised

Source: Budget 2023 People’s Guide

How much will you be paying in income, petrol and sin taxes?

Use Fin 24’s four-step Budget Calculator here to find out the monthly and annual impact on your income tax, as well as what you will pay in future in terms of fuel and sin taxes, bearing in mind that the best way to fully understand the impact of the announcements in Budget 2023 on your own and your business affairs is to reach out for professional advice from your accountant.

Budget 2023: How It Affects You and Your Business

“This is not an austerity budget. It is a budget that makes tough trade-offs in the interests of the country’s short and long term prosperity.” (Finance Minister Enoch Godongwana – Budget 2023

Finance Minister Enoch Godongwana’s second Budget contained no major tax proposals, thanks to an improvement in revenue from higher collection in corporate and personal income taxes, and in customs duties.

Instead, the focus of Budget 2023 was firmly on the current energy crisis, which has resulted in a State of Disaster being declared. It announced that government will take over R254 billion of Eskom’s debt over the next two years, subject to stringent conditions.

Of the tax relief amounting to R13 billion to be provided to taxpayers in 2023/24 announced in the Budget, R9 billion is earmarked to encourage households and businesses to invest in renewable energy. More specifically, R4 billion in relief is provided for households that install solar panels and R5 billion to companies through the expansion of the existing renewable energy incentive.

These incentives are briefly detailed below, along with some of the other announcements that will impact individuals and businesses.

Budget announcements that will impact you personally

- A new tax incentive to install rooftop solar panels: For one year from 1 March 2023, individuals will be able to claim a rebate of 25% of the cost of installing rooftop solar panels, up to a maximum of R15,000, to reduce their tax liability in the 2023/24 tax year.

- The personal income tax brackets will be fully adjusted for inflation, increasing the tax-free threshold from R91,250 to R95,750.

- Medical tax credits per month will be increased by inflation to R364 for the first two members, and to R246 for additional members.

- The retirement tax tables for lump sums withdrawn before retirement and at retirement, will be adjusted upwards by 10%, increasing the tax-free amount at retirement to R550,000.

- Revised draft legislation on the ‘two-pot’ retirement system will be published, including the amount immediately available at implementation from 1 March 2024. Withdrawals from the accessible “savings pot” would be taxed as income in the year of withdrawal.

- Social grants will increase in line with CPI inflation. The R350 grant will continue until 31 March 2024.

- Increases in the excise duties on alcohol and tobacco of 4.9%, in line with expected inflation. This means that the duty on:

- a 340ml can of beer increases by 10c,

- a 750ml bottle of wine goes up by 18c,

- a 750ml bottle of spirits will increase by R3.90,

- a 23g cigar goes up by R5.47,

- a pack of 20 cigarettes, rises by 98c.

Budget announcements that will impact your business

- Expanding the existing section 12B tax allowance for renewable energy, businesses will now be allowed to reduce their taxable income by 125% of the cost of an investment in renewables for two years from 1 March 2023. There will be no thresholds on the size of the projects that qualify. According to National Treasury, where a renewable energy investment of R1 million is made by a business, that business will qualify for a deduction of R1,25 million, which could reduce the corporate income tax liability of a company by R337,500 in the first year of operation.

- The existing Bounce Back Loan Guarantee Scheme will be updated to become the Energy Bounce Back Scheme, to be launched in April 2023. Government will guarantee solar-related loans for small and medium enterprises on a 20% first-loss basis.

- The research and development tax incentive will be extended for 10 years and will be refined to make it simpler and more effective.

- The urban development zone tax incentive will also be extended, by two years.

- Manufacturers of foodstuffs will for two years (from 1 April 2023) also qualify for the refund on the Road Accident Fund levy for diesel used in the manufacturing process, such as for generators, to ease the impact of the electricity crisis on food prices.

Budget announcements that will impact all

- Providing tax relief of R4 billion, the general fuel levy and the Road Accident Fund levy will not be increased this year. However, the carbon fuel levy will increase by 1c to 10c/l for petrol and 11c/l for diesel from 5 April 2023.

- The health promotion (sugar) levy will remain unchanged for the following two fiscal years.

- The brackets of the transfer duty table will also be increased by 10%, allowing properties below R1.1 million to avoid any transfer duty payments.

How best to manage these changes and their impact?

In addition to the announcements detailed above, there were other technical amendments proposed in the Budget review that will require professional advice.

As tax collection remains government’s main source of income, you and your business would do well to rely on the expertise and advice of tax professionals as you determine the impact of the Budget 2023 announcements on your tax affairs.