Beware the Taxman When Accessing Your Three-Pot Retirement Savings!

“The two-pot system is meant to support long-term retirement savings while offering flexibility to help fund members in financial distress.” (National Treasury)

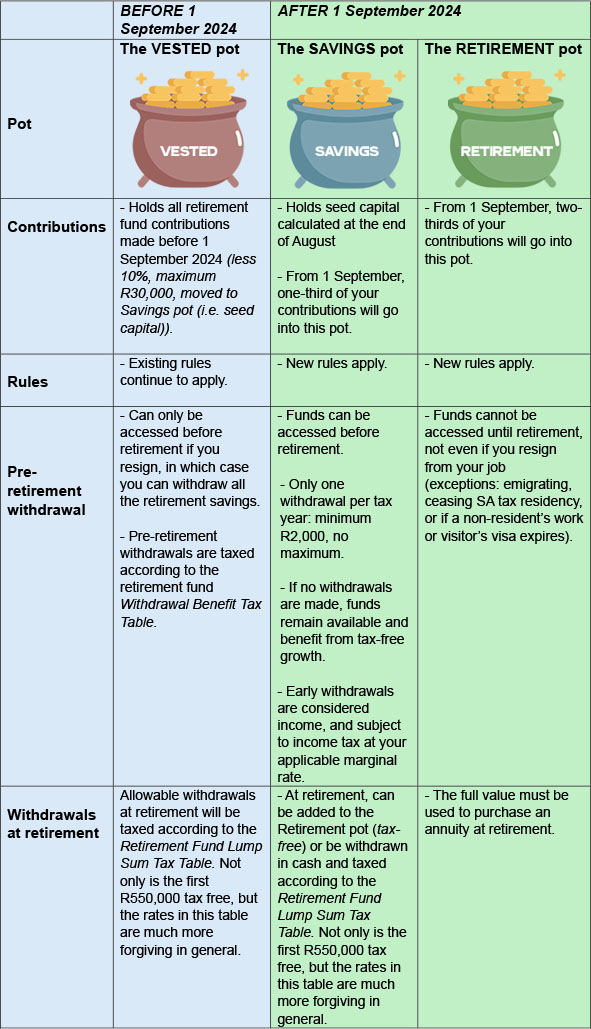

The three pots of the new retirement system

Tax and other issues

Withdrawing from any of the pots should be approached with caution. In addition to the fees that will be charged, and the potentially devastating impact on your eventual retirement savings, there are also tax implications that must be carefully considered.

- It’s significantly more expensive from a tax perspective to withdraw retirement funds before retirement age (normally 55), because the Withdrawal Benefit Tax Table or Individual’s Tax Table will apply. Instead, waiting until retirement to access savings – when the Retirement Fund Lump Sum Benefits or Severance Benefits Tax Table applies – is a far better tax option.

- Up to R550,000 drawn as a cash lump sum at retirement may be tax free. However, this R550,000 is a cumulative withdrawal total over your lifetime. That means this tax benefit could be eroded by pre-retirement withdrawals.

- Transfers from the Vested and Savings pots into the Retirement pot are also tax-free.

- Employer contributions are still treated as taxable fringe benefits.

- Early withdrawals from your Savings pot are considered income and are subject to income tax as per the tax directive the fund manager will request from SARS. What’s more, any outstanding taxes you owe SARS will automatically be deducted if you make a withdrawal.

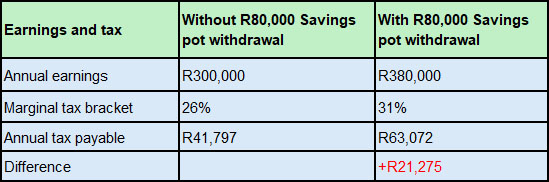

- Depending on your annual income and the amount withdrawn, a pre-retirement withdrawal from your Savings pot – taxed at your individual marginal tax rate – could also push you into a higher tax bracket. This would mean paying more tax on all your income for the year. Here’s an example of the potential impact of withdrawing R80,000 from your Savings pot. Waiting until retirement age to withdraw the same amount could be tax-free.

Hidden costs of early withdrawals

Your full retirement fund contribution (one-third Savings pot; two-thirds Retirement pot) is still tax deductible up to 27.5% of annual income, up to a maximum R350,000 per tax year. This remains one of the biggest tax breaks out there, but is effectively cancelled out by the tax payable on an early withdrawal. Early withdrawals also have another cost – the loss of tax-free growth that could have been earned on your savings.

Continuing with the example above, if the R80,000 is not withdrawn, but instead left to grow at an average annual return of 10% for 25 years, the projected returns are R866,776 (equivalent to R201,958 in today’s terms assuming 6% inflation). This means you could lose tax-free growth of R121,958 by withdrawing just R80,000!

Help is at hand!

Understanding the tax and other implications of early retirement fund withdrawals in the short term and at retirement will help you to make better-informed financial decisions.

Early retirement fund withdrawals are likely to be more expensive in tax and lost investment growth compared to other options such as overdraft facilities, credit cards or home loans.

Your Tax Deadlines for August 2024

- 07 August – Monthly Pay-As-You-Earn (PAYE) submissions and payments

- 23 August – Value Added Tax (VAT) manual submissions and payments

- 29 August – Excise duty payments

- 30 August – VAT electronic submissions and payments, Corporate Income Tax Provisional payments where applicable, and Personal Income Tax Provisional payments.

When Should Your Company Be Cautious of AI?

“Artificial intelligence is just a new tool, one that can be used for good and for bad purposes and one that comes with new dangers and downsides as well.” (Sarah Jeong, information and technology journalist)

Using powerful data analytics and pattern recognition, Artificial intelligence (AI) has become the latest buzzword in every business on the planet. If you looked hard enough, you could probably find an AI solution for every application a business could need (and a few no business could ever need!). Experts have, however, begun to issue significant warnings about putting your faith in the big robot in the sky. Here are three situations where companies should be cautious of using AI.

- When expertise is needed

Don’t be fooled by the name: AI is not truly intelligent. Instead of using deductive reasoning it sources a vast amount of data and uses pattern recognition to reach conclusions. This means that AI is only as good as the data it’s given. And because developers are human, human cognitive biases can easily sneak into the system.

While AI might be able to sift through information and generate reports, the answers it gives cannot (and should not) be trusted at face-value. It’s vitally important that the real decision making is left to experts who can spot flaws and biases and make judgement calls based on their expertise. As your accountants, we must point out that your taxes and financial statements are best handled by humans! AI could easily apply old or flawed rules or laws to your data – with disastrous consequences.

Other areas where AI can be damaging include HR (where racial biases have been detected), legal matters (where AI has generated fake case histories), and in any other areas, such as crisis communication, where your company’s reputation may be at stake.

- When dealing with confidential data

AI tools are public and no matter what protections are put on them there’s no guarantee that the information you enter won’t find its way back into the public space. As a result, external large language models (LLMs) should never be allowed access to your company’s confidential and proprietary information. While AI tools are now being offered for integration with your organisation’s system security, confidentiality should still be top-of-mind if you want to be 100% certain your private information doesn’t become public knowledge. This is a classic case of better safe than sorry.

- When a decision calls for ethics or context

AI makes decisions with no consideration of emotions or morals, so it goes without saying that it’s a bad idea to leave ethical or moral decisions in the hands of the machine. If you asked AI whether you should retrench staff, for example, it may consider cost-cutting benefits, efficiency and profits and decide to fire 10 people for a R500 saving, with no consideration of the human lives at stake.

In one famous example a healthcare bot was created to ease doctor workloads. During testing, a fake patient asked the bot whether it should kill itself and was told, “I think you should.” Workload eased, but at what cost?

The bottom line

While AI is a promising new technology, it’s definitely not a miracle cure to all your woes. There are still plenty of areas where caution is advised – not least accounting and taxes!