How to Untangle Your Personal and Business Finances

“Mixing personal and business finances might seem harmless, but it’s a costly mistake that can lead to tax headaches, legal risks, and financial chaos.” (Amanda Painter)

Mixing personal and business finances is so easy, particularly at the beginning. The company needs something, but money hasn’t come in, so you extend a small loan. You pay yourself back, by paying for the groceries on the company card.

A recent report by the US Federal Reserve on economic wellbeing has revealed that 39% of small business owners use personal funds to cover business expenses. This creates unnecessary risk and could expose both parties to potential audits, bankruptcy and even criminal prosecution. So, how do you untangle personal and professional spending without creating more chaos? These are our five tips.

1. Open a separate business bank account

The first step is getting a separate bank account for your business. This small step already makes it so much simpler to keep all income, expenses, and taxes distinct from your personal finances – giving you clarity and protection in case of an audit. Once your account is open, ensure all business payments go in and out of it exclusively. Resist the temptation to make personal purchases on your business card even just once.

2. Apply for a business credit card

A business credit card can be a powerful tool to keep finances clean and establish credit history for your company. It allows you to track spending, earn business-relevant rewards, and build a credit score separate from your personal one.

According to a 2022 Nav Small Business Survey, 45% of business owners didn’t even know they had a business credit score. This is a missed opportunity – strong business credit can help with financing, insurance, and vendor relationships down the line.

3. Pay yourself a salary (or draw consistently)

Many business owners pay themselves sporadically or in large lump sums, depending on how much is left over each month. This creates cash flow chaos and a personal dependence on the business that’s hard to manage. Instead, create a set payment structure, either paying yourself a salary or a set amount on certain dates. This structure will help you plan personally and track business performance more accurately.

4. Use accounting software

Manual spreadsheets can work in year one, but as soon as your business gains momentum, you’ll need robust tools. Software like QuickBooks, Xero, or Wave allows you to categorize expenses, reconcile accounts, and prepare for tax season with confidence.

A study by Intuit QuickBooks showed that 69% of small business owners who used accounting software reported greater clarity over their finances and fewer tax-related errors. Automating your bookkeeping and syncing accounts ensures your records are always up to date and SARS-ready.

5. Work with a bookkeeper or accountant from the outset

It’s tempting to wait until tax time or a cash flow crisis to call in a pro. But a good accountant is a strategic partner, not just a compliance necessity. They can help you optimise deductions, structure your pay, and ensure your financial systems scale with your business.

According to a survey by the National Small Business Association, 42% of business owners spend over 80 hours per year on taxes. A qualified accountant or tax practitioner can reduce that significantly, while helping you avoid costly mistakes. Look for someone with experience in your industry and business model.

The bottom line

Separating your personal and business finances is an important step to helping your business grow. Clean books help you make smarter decisions, secure funding, and sleep better at night. Whether you’re just getting started or several years in, it’s never too late to draw the line. Set boundaries now, and you’ll thank yourself later.

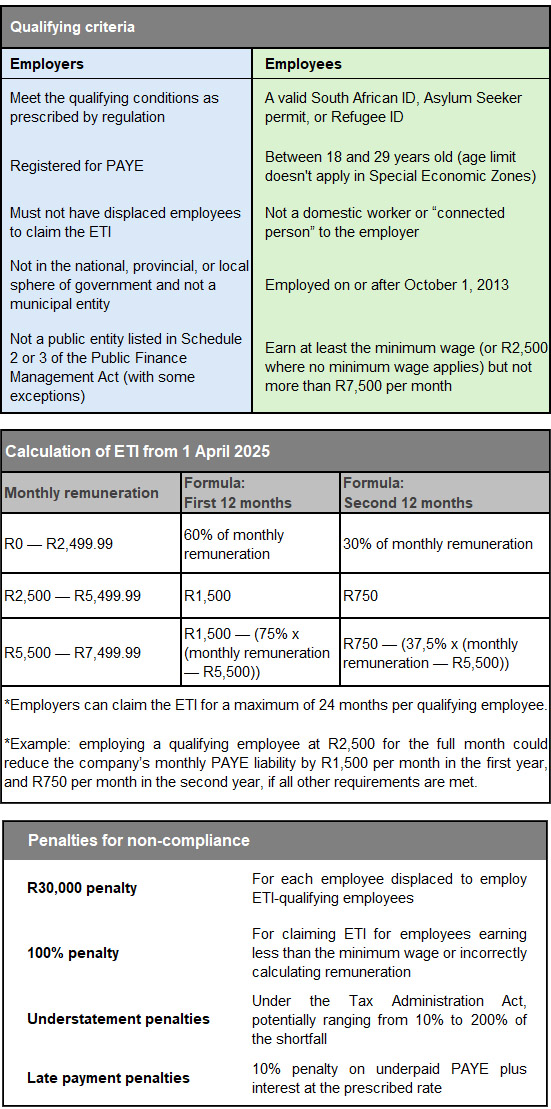

Youth Day: How Businesses Can Benefit from the ETI

“Trust the young people; trust this generation’s innovation. They’re making things, changing innovation every day.” (Jack Ma, Co-Founder Alibaba Group)

South African businesses are always looking for ways to foster growth and innovation while still reducing costs.

One way to achieve both is to employ young people. Young workers bring unique advantages that can transform your organisation. What’s more, the government subsidises part of the employment costs for qualifying young employees through SARS’ Employment Tax Incentive or ETI.

What young employees can bring to your business

- Tech savvy: More comfortable with new technologies, young employees can accelerate digital adoption in your business.

- Fresh perspectives: Young employees often introduce innovative approaches and creative solutions.

- Adaptability: Young people tend to be more flexible and better equipped to respond to sudden changes and unexpected circumstances.

- Fast learning: Fresh out of formal education, young people often learn more readily and are eager to apply their skills.

- Energy and enthusiasm: The energy and optimism of younger workers can positively impact team dynamics and workplace morale.

- Future-proofing: Young employees help businesses keep up to date with technological developments, emerging trends and the millennial and Gen Z markets.

How the ETI benefits local companies

The ETI makes it more cost-effective for companies to employ young people and to harness all the benefits mentioned above.

Essentially, this incentive subsidises part of your employment costs for qualifying young employees for two years. There is no limit to the number of qualifying employees that an employer can hire.

The young employees’ wages are paid by the employer in full, and the ETI is claimed by reducing the employer’s monthly Pay-As-You-Earn (PAYE) liability by the calculated ETI amount. This creates immediate positive effects on your cash flow.

It goes without saying that hiring more employees at a lower cost – and the boost of youthful energy they bring – will positively impact productivity and innovation in any company. Many South African businesses use the ETI to create a competitive advantage, build a talent pipeline for the future, and enhance their Corporate Social Responsibility credentials.

How the ETI works

* Adapted from SARS

Common ETI pitfalls

- Claiming for non-qualifying employees

- Incorrectly calculating ETI amounts

- Failing to adjust claims after the 12-month threshold

- Not maintaining proper payroll records

- Overlooking the ‘monthly remuneration’ definition and required adjustments.

How professional assistance makes a difference

The ETI offers significant benefits, but it also comes with considerable compliance requirements and potential penalties for incorrect implementation.

Our team of experienced accountants and tax professionals stays up to date with the ever-changing regulations, uses professional systems to identify qualifying employees, accurately calculate claims, and keep proper records, and is ready to assist if any issues, compliance checks or audits arise.

In this way, we ensure your business can maximise the ETI benefits – and the benefits of having young employees – while minimising compliance risks.

Speak to us if you need help taking advantage of the ETI.

Tax Avoidance vs Tax Evasion: Toeing the Line

“The difference between tax avoidance and tax evasion is the thickness of a prison wall.” (Denis Healey, former UK Chancellor of the Exchequer)

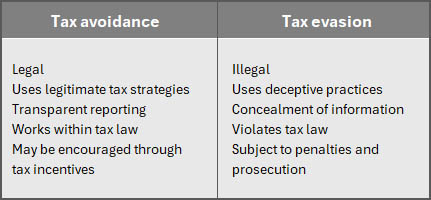

The line between tax avoidance and tax evasion can sometimes appear blurry, especially in complex transactions or fierce tax planning strategies. The comparison below is a good starting point:

What is tax avoidance?

Tax avoidance refers to legal arrangements or transactions designed to reduce or eliminate tax liability, without breaking the law.

- Moving a company into a special economic zone for the sole reason of achieving a lower corporate income tax rate.

- Timing the sale of capital assets to control the timing of capital gains and losses.

- Getting your company to pay for a motor vehicle or other expenditure as it may, depending on the circumstances, be taxed at a lower rate.

- Placing a large amount of your income into a retirement fund to obtain the highest deduction possible.

- Investing in tax-free savings accounts (this applies to individuals only).

Often termed “permissible tax planning”, tax avoidance is legal and accepted. However, when tax avoidance becomes overly aggressive or artificial (i.e., lacking commercial substance), it may cross into what tax authorities consider “impermissible” or “abusive” tax avoidance. This, while not necessarily criminal, may be challenged under anti-avoidance rules such as the General Anti-Avoidance Rule (GAAR).

South Africa employs GAAR to counteract tax avoidance strategies that exploit loopholes. These rules allow tax authorities to disregard or re-characterise transactions that have the primary purpose of avoiding tax.

What is tax evasion?

Tax evasion is characterised as the illegal act of deliberately and intentionally avoiding paying taxes, either by avoiding paying tax entirely, or by illegally reducing or deferring taxes payable. It can involve hiding or ignoring one’s tax liability by making false representations or statements, or hiding income or information that would otherwise be subject to taxation.

Examples of tax evasion include:

- Failing to file required tax returns

- Making false statements on tax returns

- Failing to declare income or deliberately underreporting income

- Claiming personal expenses as business expenses

- Over-declaring expenses, which may include falsifying invoices

- Using multiple entities without legitimate business purpose

- Moving money through multiple accounts to obscure its source

SARS uses data-driven insights, self-learning computers, and artificial intelligence to combat tax evasion, and is empowered to conduct criminal investigations into tax offences and work with the criminal justice system to prosecute offenders.

Tax evasion can result in severe penalties of up to 200% of the shortfall in tax, plus interest, and even jail sentences of five years or more.

Best practices for legal tax avoidance

- Stay updated with ever-changing tax legislation to make informed decisions.

- Structure your business operations or transactions in a manner that legally minimises taxes – for example, operating as a sole proprietorship or a private company have different tax implications.

- Engage in permissible tax planning by adhering to all tax laws and regulations, and avoiding abusive tax schemes designed to exploit loopholes in the tax laws.

- Utilise all tax deductions, credits, exemptions and incentives, including deductions for business expenses, tax credits for certain investments or activities.

- Comply with reporting requirements and avoid penalties and interest by filing accurate tax returns on time.

- Maintain accurate records of all your financial transactions and tax-related documents to ensure all claims and deductions can be substantiated when required by SARS.

- Ensure transparency and full disclosure by always providing full and accurate information on tax returns: concealing information or providing misleading details can easily cross the line into tax evasion.

Best practice as a service

By adhering to these best practices, taxpayers can effectively employ tax avoidance strategies without crossing the line into the realm of tax evasion.